The upturn in industry fortunes - which some predict will continue until 2017 - is being reflected in notable rises in tender prices, building costs, and pressure on resources

01/ Executive summary

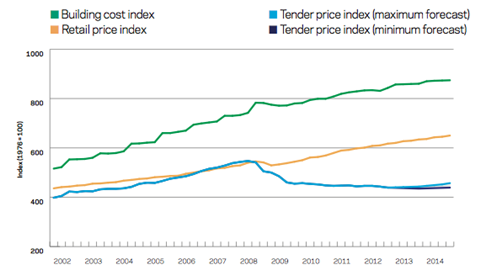

Tender price index ▲

Prices moved up at a quicker rate in the fourth quarter as a result of higher output and new orders. Stronger expectations of future price increases are becoming more commonplace.

Building cost index ▲

Higher demand for key skills and materials has accelerated the rate of annual growth. Solid demand for these materials is likely to remain in the near-term, at least until supply adjustments are made.

Retail prices index ▼

The rate of annual change slowed

to +2.6% in the fourth quarter of 2013. Inflation pressures eased

over the period for many goods, although energy prices remained broadly stable.

02/ Trends and forecasts

CIPS Markit’s UK Construction PMI print for November 2013 was its highest reading since June 2007. Six-month averages of this sentiment survey underscore the two-part story of 2013. The six-month average for the first half of 2013 came in at 48.7; the corresponding figure for the second half approached 60 (values above 50 indicate expansion). This striking turnaround in sentiment is supported by the findings of other industry surveys, where both present and future expectations for workload, orders, enquiries and pricing are all firmly positive. But there are still location and sector-specific dynamics in play.

Excess capacity throughout the industry is quickly being used up and this is amplifying the belief of changing fortunes. As the feel-good music continued to play during the last quarter of 2013, expectations of future workload brought increased recruitment activity. Securing the right resources is now a more prominent challenge on the back of increased workload.

Encouragingly, orders and workload are following on from impressive data contained within leading indicator surveys. A moving average of Barbour ABI’s index of new orders reveals a steady increase through 2013, and the highs of 2012 are almost within reach.

Looking further ahead, latest forecasts from the Construction Products Association (CPA) indicate that workload is predicted to rise to 2017. Construction output is expected to increase by 3.4% in 2014 and 5.2% in 2015, though a cautionary note is added to the CPA forecasts. The longer-term sustainability of the present industry rebound is highlighted because of “considerable uncertainties” in the wider economic landscape post-2015.

A stubbornly high UK trade deficit underlines that the much sought after balanced recovery is eluding the UK on its path to longer-term growth. Less reliance on consumer expenditure, growing exports and supporting investment are all key areas of the engine of any sustainable recovery.

Business lending data released by the Bank of England showed the biggest drop in loans to companies in more than two years in November. This news divided opinion as to whether it was a result of weak demand, banks’ reluctance to lend or simply that many corporations are sitting on large cash holdings. Construction activity is linked to business investment and any reduction in lending for investment could impact activity.

The general election in 2015 does introduce some uncertainty in respect of business investment. It is possible that part of the recent spike in construction activity is the result of decisions to construct while the investment environment is known.

The Office for National Statistics (ONS) announced that construction output in November 2013 had fallen 4% month-on-month. Perhaps the more reassuring story associated with this data release was in the three months to November compared to the same period in 2012, which showed that output increased by 5.1%.

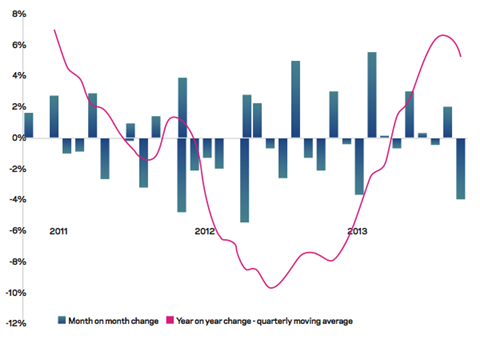

Momentum during Q4 2013 has generated a 1.1% quarterly increase in Aecom’s Tender Price Index, which measures average tender price movement for competitively tendered projects in Greater London. Analysis of tenders shows that price levels and associated confidence are beginning to percolate through other regions, although variations by sector and location are evident. Price competition that had been maintained by the lower levels of output posted in the first half of 2013 seems to have given way to a wider belief that the supply chain can and will now increase prices. Annual tender price inflation across Greater London for the year ending Q4 2014 is forecast at 2-5%; and 3-6% for the year ending Q4 2015.

Input costs continue to steadily increase, adding to existing contractor margin pressures. Analysis of recently tendered Aecom projects shows that unit rates for brickwork, blockwork and concrete have quickly adjusted to incorporate rising input costs. More generally, blockwork unit rates have increased by 25% over the last 12 months in response to demand and supply relationships.

The possibility still exists that contractor margins have not yet shown the effects of competitive bids made in recent years, particularly where projects subsequently proved to be problematic. Contractor margins may still be tight until 2015 should input costs - especially wages and salaries - increase more quickly than output prices. Additional commercial pressures will do nothing to help already exacting situations, not least when there is the prospect of new work available at better prices.

03/ Focus: Procurement

With the upturn in activity across London, changing dynamics introduce new considerations for successful project delivery. Aecom’s recent survey of main contractors operating in the commercial sector in London found that many contractors are seeking to manage their market interaction and workload in order to achieve consistency and stability. Despite this survey’s focus on the commercial sector, many of the issues are, or may become, replicable across geographies and sectors.

Although tendering activity increased in 2013, constrained delivery capacity has led to contractors becoming more selective in the projects for which they tender. Procurement complexity is likely to challenge existing ways of delivery, particularly where sectors are disproportionately affected by supply-chain pressures.

Client organisations and consultant teams must therefore invest greater effort into ensuring that their scheme attracts the best possible interest. Consideration of alternatives to the single-stage design-and-build procurement route will need to become higher on the agenda.

Some contractors believe that clients have seen the downside of single-stage design-and-build: not only were costs procured competitively but also programmes were unrealistic. In some cases, project delays have resulted because of a misalignment between time, cost and design intent.

Looking ahead, a number of stress points are anticipated. A strong trend towards selectivity of tendering has emerged as a result of the market conditions, capacity and secured work. Key considerations by contractors when deciding whether to tender include:

- The client Contractors are looking for long-term relationships, repeat business and a visible pipeline of workload. Client focus is still a critical success factor and one to which contractors pay close attention

- Competition Contractors will bid only against similar-sized companies, especially on single-stage, lump-sum contracts

- Procurement route Single-stage design and build tenders are deemed to be increasingly expensive when considered against the likely cost-to-bid and the chances of success

- Capacity Single-stage tenders are usually more resource-intensive - ample tendering opportunities therefore require commensurate staff levels. As secured work has increased, some opportunities will be declined if a project team with the right skills is unavailable;

- Tender programme Is the pre-qualification/tender period sensible for the size and scale of the project? Are key procurement stages sequential. How long is the pre-contract period to which contractors are required to commit?

- Risk profile Contract conditions and risk transferred through design and project requirements, which is deemed excessive, may result in the rejection of single-stage design and build for projects with increased risk

- Selection criteria Outlining selection criteria provides additional clarity, and is particularly important for contractors who prefer selection to be based on value as well as cost.

The assessment and pricing of risks and project uncertainties is an area where views are changing. As a result of the downturn, pricing of risk within tenders became a competitive element in some instances. As the market approaches an inflection point, tender allowances are likely to be adjusted so that risk exposure is more accurately reflected within any commercial offer. The potential exists therefore that a project’s cost increases above inflation where larger risks are assessed.

Supply chain prices are expected to increase on the back of rising profit expectations, tendering selectivity and increasing labour costs, largely brought about by labour shortages. On this issue, bricklaying, concrete, other domestic trades and M&E have all been cited as skills areas that are expected to see above average rates of cost inflation. Trades with sector overlap are displaying strong demand growth, with suggestions that some are overheating. Similarly, contractor staff costs and rising senior level salaries are featuring more often within project and business planning processes, as contractors seek to retain and recruit skilled people.

Successful delivery in a transitioning market requires clear thought and good planning. Some key factors include:

- Allocating a sensible time frame for pre-qualification and the tender period, and ensure contractors are notified in advance to enable allocation of bid resource;

- Providing clear tender information - quality documentation is emphasised, as opposed to quantity

- Offering equitable contract conditions, along with contract mechanisms that have positive impacts on tender price and the overall commercial offer

- Innovative use of single-sourcing or two-stage tendering with incentives and risk sharing

- Including early trades to secure some element of fixed price in the first stage.

Many contractors continue to manage challenges ranging from working capital, organisational restructuring, wage inflation, skills retention and operational delivery. Behind this all though is an acknowledgement that applying a client focus will pay off through repeat business and contract extensions. But the terms of engagement may be quickly shifting as the market moves to its next phase.

With thanks to Brian Smith of Aecom

04/ Activity indicators

Construction’s annual growth rate slowed to 2.2% in November 2013, down from 5.1% in October, according to the Office of National Statistic’s latest data release. The slackening in growth rate was the sharpest contraction seen in 2013, and was experienced across construction sectors. New work returned a 3.9% fall month-on-month, which was largely attributed to a 7.1% decline in private commercial new work and reductions in private new housing (-3.2%) and new infrastructure (-4.8%).

Removing noisy monthly data reveals broader underlying trends in output. A comparison of September-November 2013 with the previous three-month period highlights a 0.7% increase. Similarly, all work during September-November 2013 increased by over 5% when compared with the same period in 2012. Further volatility in near-term monthly output data could follow as a result of recent adverse weather and flooding that affected parts of the UK.

Most activity indicators continue to report strong sentiment and confidence across the industry, despite a slight reversal in the latter months of 2013. Future scenarios for pricing, activity and employment prospects are also generally positive. The Federation of Master Builders’ latest trade survey shows that enquiries, workload and employment prospects have improved notably for small and medium-size enterprises (SMEs) - and this is reflected across most parts of the UK. Two-thirds of SMEs expect material costs to increase and, similarly, that output prices will rise in response to advancing wages and salaries, materials costs and the perceived likelihood of securing better prices.

More signs of construction industry confidence were revealed in the ICAEW/Grant Thornton UK Business Monitor Q4 2013 survey. The construction and property sectors topped the rankings of individual industries and also composite measures. Construction’s dramatic turnaround from a print of -3.9 in Q4 2012 to +37.8 in Q4 2013 underscores the sharp change in outlook across the industry.

Additionally, construction sector business insolvencies fell for the 10th consecutive month, according to Experian.

05/ Building cost index

Aecom’s building cost index rose 3% year-on-year in Q3 2013. High demand for key materials, such as bricks and blocks, has resulted in a spate of recent price rises. Bricks and block increases ranged from 5-10%, while announcements for ready-mix concrete increases were between 3-5% depending on quantity.

Renewed housebuilding activity spurred a significant increase in production and delivery of bricks in the UK during the second half of 2013. Brick production expanded by over 12% in Q3 versus the same quarter in 2012. Meanwhile, deliveries rose by nearly 20% as stocks were drawn down. Because of the recessionary slump in construction demand, the number of operational brickworks fell to 50, from 80 in 2007. However, previously moth-balled brick kilns have been fired back to life in response to rising demand from housebuilders. Additionally, many producers are now operating over the winter months, reversing a practice of idling production facilities or reducing capacity over this period.

A recent data release by the Department for Business, Innovation and Skills outlines a growing trade gap between the value of imported building materials and corresponding exports. Imports rose quicker than exports in Q2 2013 when compared with the first quarter, accelerating the divergence.

Any further appreciation in sterling will not aid this situation as exports become more expensive; conversely, imports become cheaper which has possible benefits at project or programme level but not necessarily for the UK.

Commodity prices generally continued trends established through 2013. Annual averages for aluminium and copper in 2013 were approximately 10% lower than 2012, while iron ore moved upwards, finishing 5% higher than 2012 average figures. Short to medium-term forecasts by the World Bank indicate negligible increases in

many metals commodity prices (nominal terms).

However, energy prices generally climbed by over 3% in December 2013, according to World Bank indices. Further energy price rises will add to the operational costs of both energy-intensive manufacturers of building materials and contractors. Whether these higher costs propel the speed of future price increases will become clearer in the early months of 2014, particularly if a prevailing trend of building price inflation is under way.

Labour rates are responding to immediate higher demand. Additional workload and improving confidence only adds to the likelihood that labour rates will increase if supply remains restricted and workload accelerates. Some attention has turned to the use of imported labour, mostly from the EU, in order to respond to demand peaks. Such a resourcing response could though temper wage inflation for skilled labour more generally.

Pay deals were recently agreed for workers covered by the Construction Industry Joint Council (CIJC). Pay rates will increase by 3% from 30 June 2014, and a similar rise is secured from June 2015. Travel allowances also increase from June 2014, while subsistence allowances increase immediately from January 2014.

No comments yet