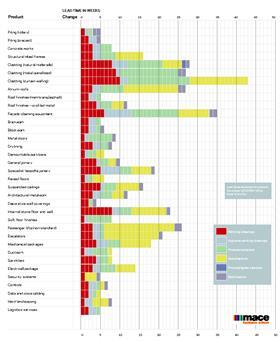

Lead times remain extremely low and static across all trades, with rotary piling and facade cleaning the only packages showing any movement

01/Staying level

Sprinklers

Pre-cast piling

Concrete works

Structural steel frames

Cladding (reconstituted stone)

Cladding (natural materials)

Metal panellised cladding

Curtain walling

Atrium roofs

Asphalt/membrane roof finishes

Profiled metal roof finishes

Brickwork

Blockwork

Drylining

Metal doors

Demountable partitions

General joinery

Specialist joinery

Raised floors

Suspended ceilings

Architectural metalwork

Decorative wall covering

Internal stone floor and wall finish

Non-standard passenger lifts

Escalators

Electrical packages

Ductwork

Security systems

Controls

Logistics services

Soft floor finishes

Mechanical packages

Hard landscaping

02/ Going down

Rotary piling

Facade cleaning equipment

03/ Lead times summary

Rotary piling lead times have fallen by three weeks to five weeks since last quarter. This follows an increase over the previous two quarters and now returns to just below levels reported at the end of 2011. Pre-cast piling has remained stable at five weeks since 2008; contractors are reporting that workload is busier than the past six months but no change is anticipated.

Concrete works remain at eight weeks following the increase last quarter. Structural steel frames have been at the same level since they increased to 16 weeks over a year ago.

Cladding - natural materials has been at 28 weeks since the beginning of 2011. The potential mothballing of production facilities at material suppliers is being reported, and busier workload could lead to an increase over the next six months. Metal panellised cladding have been at 27 weeks since Q1 2010 and no change is forecast. Curtain walling cladding continues to be busier than six months ago but no increase is forecast.

Atrium roofs have remained stable at 27 weeks since Q2 2008 with no change forecast. Asphalt/membrane roof finishes have been at 5 weeks since the end of 2009 with no change forecast. Profiled metal roof finishes have stayed at 12 weeks since mid-2009, there is no change forecast for the next six months.

Facade cleaning equipment has reduced by three weeks to 35 weeks. Brickwork stays at five weeks. Most companies are reporting that the workload has stabilised but enquiries are lower. Blockwork stays at six weeks.

Drylining is stable at eight weeks, with no change forecast. Demountable partitions have remained at six weeks since the end of 2009. No change is forecast in the next six months.

General joinery remains at 10 weeks - as it has since mid-2008, with no change forecast. Specialist joinery has stabilised at 19 weeks with no change reported.

Raised floors are static at six weeks with no change since 2007. Suspended ceiling companies are generally busier but lead times remain at 16 weeks with no increase anticipated for the next 6 months.

Architectural metalwork has been static at 12 weeks for more than a year. Decorative wall covering remains at four weeks.

Internal stone floor and wall finishes stay at 23 weeks despite being busier than six months ago; enquiries are also up but no increase is forecast. Soft floor finishes have remained at eight weeks since the end of 2010.

Passenger lift - non standard remain at 26 weeks; workload and enquiries remain consistent with no change forecast. Escalator workload and enquiries remain at 21 weeks.

Electrical packages have been at 14 weeks since mid-2009, with no change forecast for the next six months. Mechanical packages remain at 18 weeks; most contractors report a reduction in workload over the next six months, but do not forecast any further reduction in lead times. Ductwork remains at eight weeks with no change forecast.

Sprinklers remain at eight weeks, with no changes forecast. Security systems have been at five weeks for over two years. Controls have been restated at seven weeks based on the availability of better information.

Hard landscaping remains at eight weeks, with no change forecast. Workload and enquiries continue to be down.

Logistics services remain at five weeks with no change forecast in the next six months.

Many contractors are reporting an increase in their workload but anticipate that lead times will stay the same over the next six months. Most contractors appear to be absorbing increases to help secure workload. Only rotary piling and facade cleaning are reporting a decrease in lead times - most other packages remain at an all-time low. In the case of rotary piling this appears to have been the result of a spike caused by the infrastructure projects in the London area over the past few months.

Data capture and analysis by Mace Business School. For more details on the article and contributors, please visit www.macebusinessschool.co.uk/foresite

No comments yet