Costs continue to rise steadily, as a result of ongoing domestic demand for materials and labour. Jay Kotecha of Aecom reports

01 / Key changes

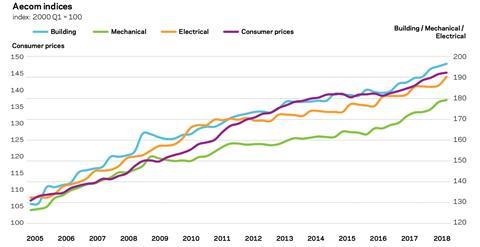

Building cost index

A composite measure of building costs increased by 3.6% over the previous 12 months. Materials costs remained a significant driver of cost inflation to the overall index. Primarily, this stems from sound ongoing domestic demand and sterling being weak against the euro and the dollar, which introduces inflationary pressures from consequently higher cost imported materials and components. Labour costs also continued to rise steadily over the first quarter of 2018, despite a brief lull where inclement weather affected wages.

Mechanical cost index

The rate of annual growth slowed to 3.5% in Q1 2018. Labour and materials components of the index maintained steady rises but some inflationary pressures have eased, with the effects of sterling’s devaluation diminishing somewhat and overall demand slipping as construction output weakens.

Electrical cost index

The index rose by 2.6%, marking an increase in the rate of change, probably stemming from a pick-up in global metals commodity prices during 2017. Demand has stayed strong, adding to the prevailing cost trends.

Consumer prices index

Consumer price inflation slowed in the first quarter of 2018 but remains above its target rate of 2%. It is expected to stay elevated through 2018, as sterling continues its “lower for longer” trend against other key currencies.

The chart shows Aecom’s index series since 2005, reflecting cost movements in different construction industry sectors and consumer prices.

Percentage change year-on-year (Q1 2017 to Q1 2018)

| % | Direction | |

|---|---|---|

| Building cost index | +3.6 | ▲ |

| Mechanical cost index | +3.5 | ▲ |

| Electrical cost index | +2.6 | ▲ |

| Consumer prices index | +2.8 | ▲ |

(Q1 2018 figures are provisional)

02 / Price adjustment formulae for construction contracts

rice adjustment formulae indices, compiled by the Building Cost Information Service (previously by the Department for Business, Innovation and Skills), are designed for the calculation of increased costs on fluctuating or variation of price contracts. They provide guidance on cost changes in various trades and industry sectors – ie those including labour, plant and materials – and on the differential movement of work sections in Spon’s price books.

The 60 building work categories recorded an average increase of 3.7% on a yearly basis. The six highest increases were recorded in the following categories:

Price adjustment formulae

| May 2017 – May 2018 | % change |

|---|---|

| Metal: decking | 9.0 |

| Concrete: reinforcement | 8.5 |

| Piling: steel | 7.6 |

| Cladding and covering: fibre cement | 7.6 |

| Windows and doors: steel | 7.6 |

| Raised access floors | 6.9 |

The other changes were as follows (only one category recorded a decline and one no change):

| May 2017 – May 2018 | % change |

|---|---|

| Cladding and covering: aluminium | -3.3 |

| Cladding and covering: lead | 0.0 |

| Pipes and accessories: aluminium | 0.5 |

| Finishes: bitumen, resin and rubber flooring | 0.7 |

| Windows and doors: hardwood | 1.2 |

| Finishes: screeds | 1.4 |

Materials

03 / summary

- Consumer price inflation increased by 2.4% in April 2018 compared with the same month a year earlier ▲

- Manufacturing input prices increased 5.3% in the year to April 2018 ▲

- Factory gate prices (output prices) rose 2.7% in the year to April 2018 ▲

- Commodity prices maintained an upwards trajectory in Q1 2018, although the rate of change has slowed ▲

- Construction materials prices continued to increase on an annual basis in Q1 2018 as a result of continuing demand and sterling weakness ▲

04 / Key Indicators

Construction industry

The BEIS All-work materials price index increased by 4.9% in the 12 months to March 2018. Housing-related materials increased by 5.2% over the same period. Non-housing materials prices also rose by 4.8% annually. All M&E categories posted significant yearly increases.

| Construction materials | % change Mar 2017 – Mar 2018* | |

|---|---|---|

| New housing | 5.2 | ▲ |

| Non-housing new work | 4.8 | ▲ |

| Repair and maintenance | 5.3 | ▲ |

| Mechanical services materials | % change Apr 2017 – Apr 2018* | |

|---|---|---|

| Housing only | 7.1 | ▲ |

| Non-housing | 3.5 | ▲ |

| Electrical services materials | 3.0 | ▲ |

| Materials showing largest cost movement | % change Mar 2017 – Mar 2018* | |

|---|---|---|

| Concrete reinforcing bars (steel) | 13.8 | ▲ |

| Imported plywood | 8.3 | ▲ |

| Imported sawn or planed wood | 7.4 | ▲ |

| Insulating materials | 6.6 | ▲ |

| Paint (aqueous) | 6.0 | ▲ |

| Builders woodwork | 4.2 | ▲ |

| Pipes and fittings (flexible) | 4.2 | ▲ |

| Pipes and fittings (rigid) | 3.9 | ▲ |

| Data sources: ONS and BEIS *provisional |

UK economy

| Consumer prices | % change Apr 2017 – Apr 2018 | ||

|---|---|---|---|

| Consumer Prices Index (CPI) | 2.4 | ▲ |

Consumer price inflation including owner-occupiers’ housing costs was 2.2% in the 12 months to April 2018. This marks a further slowing in the rate of change. Inflationary pressures remain from motor fuels, which rose between March and April 2018. Lower sterling rates will continue to add pressure to raw materials costs for UK supply chains.

| Industry input costs | % change Apr 2017 – Apr 2018 | |

|---|---|---|

| Materials and fuels purchased by manufacturing industry | 5.3 | ▲ |

| Excluding food, beverages, tobacco and petroleum industries | 5.2 | ▲ |

Input costs increased by 5.3% on a yearly basis up to April 2018. This reflects a marginal pick-up in the rate of change after a slower period of input cost increases over Q1 2018. The largest upward contributions came from crude oil and metals, both of which tend to be imported and are therefore subject to the effects of weaker sterling.

| Industry output prices | % change Apr 2017 – Apr 2018 | |

|---|---|---|

| Source: ONS | ||

| Output prices of manufactured products | 2.7 | ▲ |

| Excluding food, beverages, tobacco and petroleum | 2.4 | ▲ |

Factory gate prices increased by 2.7% on a yearly basis to April. The largest upward contribution from non-food items was from petroleum products. This 12-month rate of change continues a downward trend for output prices, although still positive and below the corresponding trend for input costs.

| % change Apr 2017 – Apr 2018 | ||

|---|---|---|

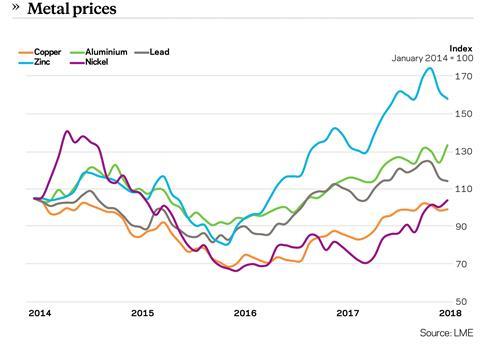

| Aluminium | 16.3 | ▲ |

| Copper | 20.0 | ▲ |

| Lead | 5.6 | ▲ |

| Zinc | 21.2 | ▲ |

| Nickel | 44.1 | ▲ |

Although commodity prices rose significantly on a yearly basis, the pace of change slowed in response to more uncertainty around global economic activity and associated geopolitics. Rhetoric and action in respect of tariffs for major economies are likely to have a knock-on effect on metals prices. There will be an immediate reaction to the events that will affect metals prices in the short run. Further movements in price trends will play out through 2018, as the impact of the tariffs and retaliatory measures begin to influence overall levels of global economic activity, along with any supply responses around domestic metals production.

| May 2017 average | May 2018 average | % change | |

|---|---|---|---|

| GBP / EUR | 1.1696 | 1.1391 | -2.6 |

| GBP / USD | 1.2933 | 1.3488 | 4.3 |

Sterling lost significant ground against the US dollar recently. Stronger economic growth and a higher probability of bank rate increases in the US make the dollar a preferable currency holding to sterling. Persistent uncertainty for the UK in respect of its political and economic outlook does nothing to help sterling’s apparent attractiveness either. Against the euro, sterling has made little or no progress in moving away from its prevailing level.

Labour

05 / Labour market statistics

- Average weekly earnings (total pay including bonuses) in construction rose to £613 in March 2018, from £605 a month earlier. Annually, total earnings increased 5.9% to March on a single-month basis. Regular pay (excluding bonuses and arrears) rose to £585 per week in March, from £580 a month earlier.

- Construction industry regular pay rates maintained their lead over average earnings for the UK economy, rising by an average of 4.6% for the three months to March 2018 versus 2.9% for the whole-economy classification.

- Real average weekly earnings for the whole economy increased by 0.4% (regular pay) for the three-month average to March 2018 compared with the same period in 2017.

Aecom’s cost indices track movements in the input costs of construction work in various sectors, incorporating national wage agreements and changes in materials prices as measured by government index series.

They are intended to provide an underlying indication of price changes and differential movements in the various work sectors but do not reflect changes in market conditions affecting profit and overheads provisions, site wage rates, bonuses or materials’ price discounts/premiums. Market conditions and commentary are outlined in Aecom’s quarterly Market Forecast (last published February 2018).

No comments yet