The decline in construction activity slowed in December, according to Experian Economics, but a low orders index and the weakest tender enquiries figures for nearly two years do not augur well

01 / THE STATE OF PLAY

The construction activity index increased by five points to 47 in December, which suggests a slowdown in the rate of decline. On a sectoral basis, residential activity saw the greatest increase, rising by 12 points to 52 - pushing back into positive territory for the first time since August 2011. The civil engineering and the non-residential sectors also saw increases in their indices, to 41 and 48 points respectively

Orders were below normal for the time of year, with the index remaining unchanged at 43. The tender enquiries index, meanwhile, fell by one point to 45, which is the lowest reading since April 2010. The non-residential orders index rose by one point to 56 in December - the only measure to record growth - while civil engineering orders’ one-point rise could not disguise the fact that it was still deep in negative territory, at 35. The residential orders index remained unchanged at 38.

The general upward trend of the tender prices index remains undented, as the measure is unchanged at 50, indicating that construction firms expect to charge the same prices over the next three months.

In December the percentage of respondents reporting no constraints on activity was 16%, decreasing for the fifth consecutive month. The proportion of firms reporting that insufficient demand was constraining their activity increased by three percentage points to 60%, which is the highest reading since our records began in 1995. About 5% of businesses saw bad weather as a limitation of activity.

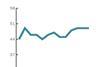

02 / LEADING CONSTRUCTION ACTIVITY INDICATOR

CFR’s Leading Construction Activity Indicator is predicted to decline in January and February 2012. The index is expected to rise by six points in March, but it will remain in negative territory at 48.

The indicator uses a base level of 50: an index above that level indicates an increase in activity, below that level a decrease.

03 / WORK IN HAND

During December 2011, about 67% of respondents in the residential sector reported less than three months’ work in hand, while for non-residential and civil engineering firms this was 57% and 55% respectively. The civil engineering sector saw the highest proportion of respondents (45%) reporting that they had enough work to keep them active for between three and six months.

Civil engineering was also the only sector to report that no work was readily available after six months. About 9% of residential firms reported that they had more than six months of work in hand, while for non-residential respondents this was about 8%.

04 / REGIONAL PERSPECTIVE

Experian’s regional composite indices incorporate current activity levels, the state of order books and the number of tender enquiries received by contractors, in order to provide a measure of the relative strength of each regional industry.

In December, only Wales saw its index rise when compared with the previous month. The measure increased by three points to 44; however, it still remained in negative territory.

Scotland saw the greatest decline in its index, which fell by six points to 41. Northern Ireland followed closely behind as its index fell by five points to 35, a reading not seen since February 2009.

Yorkshire and Humberside saw its measure fall by four points; however, it remained above the no-change mark of 50 for the seventh consecutive month.

The East Midlands’ index fell by three points to 40, while the North and the North-west both saw their indices fall by two points.

The West Midlands, the South-east, the South-west and East Anglia all saw their indices fall by one point.

As a whole, the UK index, which includes firms working in five or more regions, increased by three points, above the no-change mark to 52.

No comments yet