The construction activity index fell by a point in May following a brief peak in April, while individual sub-sectors enjoy mixed fortunes

01 / State of play

The construction activity index fell by a point to 55 in May, following April’s short-term peak. The repair and maintenance (R&M) index remained entrenched in contraction territory (47) for the third

successive month.

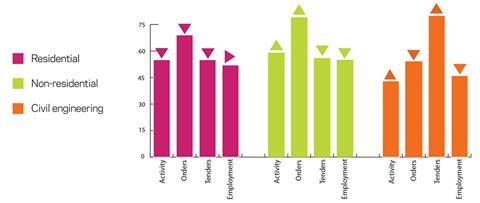

Both the non-residential and civil engineering sub-sectors experienced increases in their respective activity indices in May. The former increased by two points to 59, its highest value since February 2015. The latter picked up by one point to 43, remaining below 50 for the fourth successive month. In contrast, the residential sector fell by five points to 55.

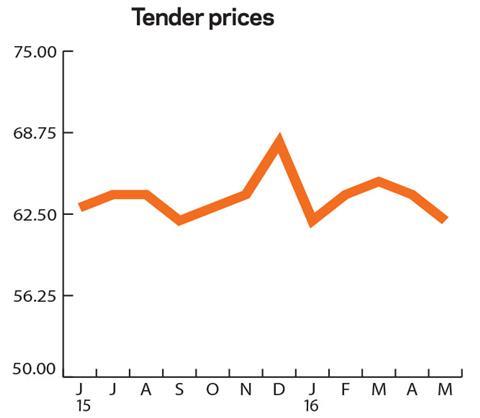

The orders index fell three points, but at 70 it remains firmly in expansion territory. It was also up four points on May 2015. Tender enquiries fell by five points to 56, but similarly the index sits comfortably above the no-change mark of 50.

For the third month in a row, over 40% of our panel of construction firms reported no constraints in construction activity. Problems regarding insufficient demand picked up, with a proportion of 35.1% citing this as an issue; this is higher than the 29.9% reported in May 2015. Concerns regarding finance similarly ticked upwards to 11.9%. For the first time since August 2014, there were no responses concerning activity constraints regarding the weather. There was a large fall in reports of labour shortage (5.3%), whereas material/equipment shortage (3.3%) picked up from no reports in April.

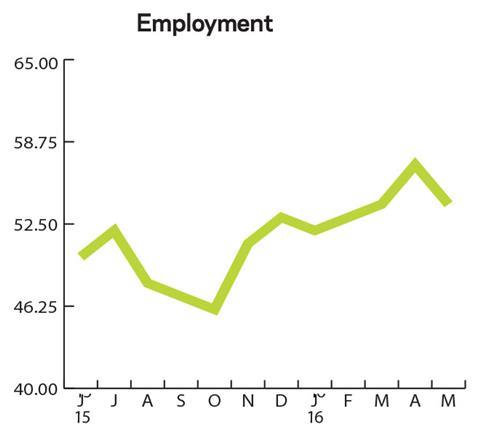

The employment prospect index fell by three points in May. However, it was up by one point to 54 on a three-month moving average basis.

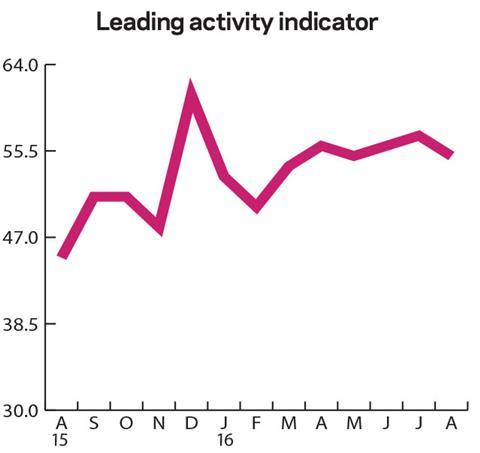

02 / Leading construction activity indicator

The CFR’s Leading Construction Activity Indicator ticked downwards by a single point to 55 in May. We expect it to lose further ground in the three months to September.

The indicator uses a base level of 50: an index value above that level suggests an increase in activity, while one below it highlights a decrease.

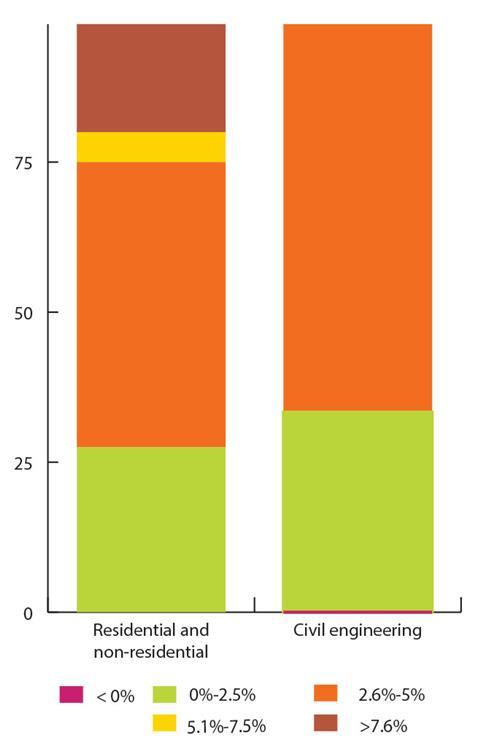

03 / Material costs

During May none of our non-residential and residential respondents reported material cost deflation. A proportion of 27.5% noted inflation between 0% and 2.5%, with 47.5% mentioning material costs increasing between 2.6% and 5% from May 2015. A following 5% noted a rise between 5.1% and 7.4%, and the remainder reported inflation over 7.5%.

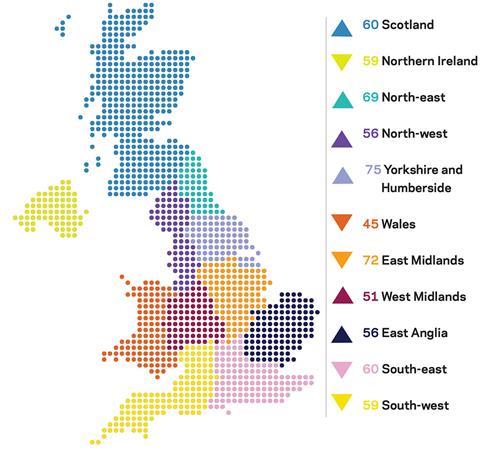

04 / Regional perspectives

Experian’s regional composite indices incorporate current activity levels, the state of order books and the number of tender enquiries received by contractors to provide a measure of the relative strength of each regional industry.

The North-west’s activity indexed outperformed all other regions in May in terms of month-on-month growth, after posting a seven-point gain, taking it above 50 points for the first time in three months. There were considerable increases for both the West Midlands (51) and Yorkshire and the Humber (75), up by six points, with the latter recording its highest value since October 2015. The North-east showed continued strength as it increased by three points, meaning the region’s index has had 16 consecutive monthly values above 50. The remaining increases occurred for East Anglia (56) and Scotland (60), with both indices increasing by a single point. In contrast, Wales (45) weakened by eight points in May, falling notably below its average level for the majority of the first half of 2016. However, the index did spend the majority of 2015 in contraction territory. The South-west (59) and Northern Ireland (59) fell by two points in May, whereas the South-east (60) and East Midlands (72) edged down by one point apiece, although both regions remained comfortably above the no-change mark.

The UK index, which looks at firms in five or more regions, fell again in May, this time by nine points to 58. This is the lowest value recorded since the turn of the year.

This an extract from the monthly Focus survey of construction activity undertaken by Experian Economics on behalf of the European commission as part of its suite of harmonised EU business surveys.

The full survey results and further information on Experian Economics’ forecasts and services can be obtained by calling 0207-746 8217 or logging on to www.experian.co.uk/economics

The survey is conducted monthly among 800 firms throughout the UK and the analysis is broken down by size of firm, sector of the industry and region. The results are weighted to reflect the size of respondents. As well as the results published in this extract, all of the monthly topics are available by sector, region and size of firm. In addition, quarterly questions seek information on materials costs, labour costs and work-in-hand.

No comments yet