Construction activity fell to a nine-month low in November as residential and civil engineering work plummeted, according to latest figures from Experian Economics

01 / THE STATE OF PLAY

The construction activity index declined for a third successive month in November 2011, falling by two points to a nine-month low of 43. The residential activity index dropped by seven points to 41, while the activity index for the civil engineering sector fell by five points to 34, its lowest level since March. In contrast, the non-residential activity index remained unchanged at 44.

Orders remained below normal for the time of year as the index fell one point to 43, highlighting the weak prospects for the construction industry. Again, it was the residential and civil engineering sectors that saw falls in their new orders indices, while the index for the non-residential sector remained unchanged at 55, signalling that orders in the sector were again above normal for the time of year.

After a brief increase in the tender prices index to the no-change mark of 50 in October, it has returned to negative territory, declining by four points to 46. Once again, firms are expecting the prices they charge to decrease over the coming three months.

Employment prospects continue to be downbeat, with the index falling by four points to 33, a six-month low.

The percentage of respondents reporting no constraints on activity was 17%, decreasing for the fourth consecutive month. The proportion of firms indicating that insufficient demand was constraining their activity also fell, edging down by two percentage points to 57%. About 3% of businesses saw bad weather as an activity constraint, a level last seen in February 2011.

02 / LEADING CONSTRUCTION ACTIVITY INDICATOR

![]()

![]()

CFR’s Leading Construction Activity Indicator is predicted to move in an upward direction over the next three months. Despite this move the index will remain in negative territory and in January 2012 the index is expected to be 46.

The indicator uses a base level of 50: an index above that level indicates an increase in activity, below that level a decrease.

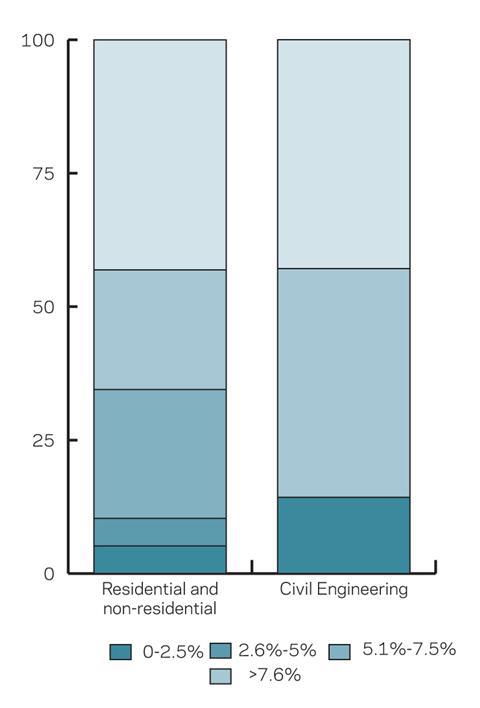

03 / MATERIAL COSTS

In November 2011, 43% of residential and non-residential firms reported that material costs had increased by more than 7.6%, year on year, an increase from the 33%in November 2010. However, in May 2011 an even greater proportion of respondents - 61% - reported annual material cost inflation of more than 7.6%.

The proportion of building firms indicating that material costs had risen, on an annual basis, by between 5.1% and 7.5% was 22% in November 2011, compared with 7% in November 2010.

In November 2011, 43% of civil engineering respondents reported that material costs had increased by more than 7.6% while another 43% stated that material prices had risen between 5.1% and 7.5% when compared with a year ago. A relatively small proportion of civil engineering firms - 14% - reported that there was a fall in the price of materials.

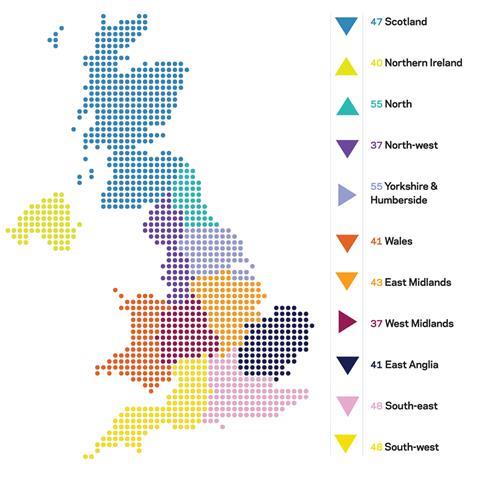

04 / REGIONAL PERSPECTIVE

Experian’s regional composite indices incorporate current activity levels, the state of order books and the number of tender enquiries received by contractors to provide a measure of the relative strength of each regional industry.

In November just two of the 11 regional indices increased. The North and Northern Ireland both saw their indices increase by three points to 55 and 40 respectively.

In total, seven regions saw a decline in their indices, while two - Yorkshire & Humberside and the West Midlands - saw no change, remaining at 55 and 37 respectively.

The greatest falls occurred in East Anglia (41) and the South West (48) where the indices both decreased by five points.

The South-east followed closely behind as its index fell by four points to 48. This is the first time the index has been in negative territory since March 2011.

The North-west (37) saw its index fall by two points while the indices for the East Midlands (43), Wales (41) and Scotland (47) all dropped by one point.

As a whole the UK index, which includes firms working in five or more regions, remained unchanged at 49 for the third consecutive month.

No comments yet