The recent changes to Part L could add up to 8% to the capital cost of building, says David Holmes of Davis Langdon. This is what that will mean for primary schools, social housing and small industrial units

01 / Introduction

The 2010 amendments to Part L are likely to increase capital expenditure by between 5% and 8%, depending on the building type. The main changes to Part L are well documented. However, it is worth underlining some of them.

For new buildings, the carbon emission rates must be calculated before work begins and given to the building control body, along with a list of the specifications used.

The annual emission rate of a completed dwelling must not exceed the target set by reference to a notional dwelling with an additional overall improvement of 25% relative to the 2006 standards.

For new non-dwellings, we still have the same five criteria for compliance, with some minor changes to each. The biggest change is to the TER (target CO2 emission rate) where an aggregate 25% reduction has been set.

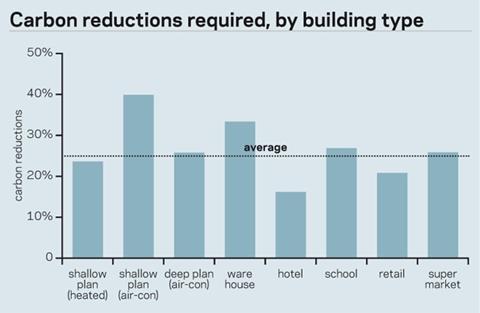

The notional building used to determine this is the same size and shape as the actual building, constructed to a concurrent specification and with no improvement factor. Previously, a notional building and an improvement factor were used. As a result some types will be required to improve by more than 25% and some less (see graph).

It should still be possible to comply with the new regulations using traditional construction methods, albeit with an increased focus on detail and quality. There are no specific requirements to incorporate renewable energy sources.

The percentage CO2 reductions required of non-domestic buildings is 25%, but emission reductions vary widely depending on the type of building

02 / Current market conditions

As reported in last week’s market forecast (29 October, page 56), workload benefited from a bounce in activity in the first half of the year and this halted the decline in

prices that has continued since mid-2008.

Workload increased in all sectors, most noticeably those where the government was involved. For instance there was a surge in school building as the previous administration brought forward work begun as part of its economic stimulus package.

The momentum continued into the third quarter of this year, where it contributed greatly to the rise in GDP. However, it is doubtful that this is sustainable, given the cutbacks announced as part of the Comprehensive Spending Review. More likely the volume of output in 2011 will be lower than in 2010 as any upturn in private sector work is unlikely to be enough to offset the fall that is about to start in the public workload.

In general construction prices have dropped about 18% since the first half of 2008. They stabilised in the first half of this year, partly because of the increase in activity, but also because of rising materials prices.

Steel prices were the primary driver here, and buildings with an above-average proportion of steel, such as portal-framed industrial buildings, became more costly in the spring. Steel prices have since started to ease and prices in general are forecast to moderate as the year draws to a close.

Prices in the South-east, excluding the effects of the Building Regulations, are expected to bottom out in last quarter of this year and the first of next. They may drift for longer elsewhere as the public sector cuts have a more disproportionate effect on industry activity and the private sector is slower to grow.

03 / Primary schools

The Primary Capital Programme, first announced in 2005, had the long-term aim of renewing at least half of all primary school buildings by 2022/23 and was supported by £1.9bn of capital investment in the period 2008-11.

By August 2010, 65 new-build schemes had been completed under the scheme, together with 128 large extensions or refurbishments. However, with the arrival of the new government, the programme came under review, along with the rest of the Department of Education’s capital investment programmes.

In July, the £55bn Building Schools for the Future (BSF) programme was axed. Only those projects that had reached financial close were allowed to continue, along with a handful

of schemes that were close to this stage. All other BSF projects, covering nearly 700 schools, were cancelled.

In the spending review, the chancellor announced that the schools budget would increase in real terms in each year of the review period but that capital spending would be reduced by 60% in real terms by 2014/15. The government is anxious to point out that the average annual capital budget over the period will be higher than in the 1997/98 to 2004/05 period.

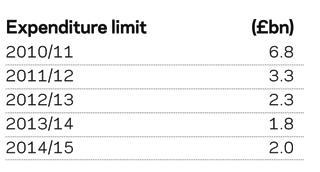

Department for Education Capital expenditure limit

The government’s independent Schools Capital Review is intended to ensure that the capital budget is “allocated in the most cost-effective way and targeted where there is most need”, but will not report until near the end of the year.

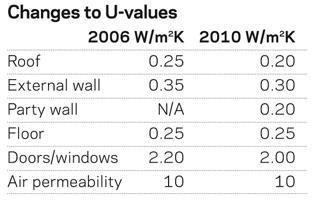

Schools built to the 2006 Part L Building Regulations were able to achieve compliance via energy-efficiency measures alone, such as more insulation and more efficient boilers.

From 1 October 2010 compliance became more difficult and a more holistic design and operation approach had become necessary. Client education will be needed to ensure users appreciate the concepts developed, and their limitations will be an important aspect of efficient project delivery.

The cost model is a single-storey, three-classroom extension to a primary school built using traditional brick cavity walls on strip foundations with pitched tiled roofing. Subdivision is by load-bearing, blockwork partitions. Services include heating, hot and cold water and some limited extract ventilation.

04 / Affordable housing

Construction activity in the public housing sector surged in the first half of 2010. Output was worth £2.2bn, a rise of 50% in real terms compared with the same period of 2009. This was largely owing to the success of the Homes and Communities Agency’s Kickstart programme, and the volume of work was maintained at an even higher rate in July and August.

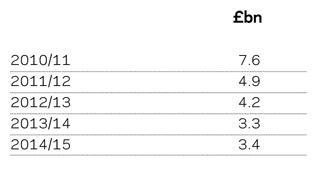

However, the communities department’s budget was the hardest hit in the spending review. Capital spending will fall as follows:

Despite the huge cuts in funding for social housing that these figures imply, the government hopes that making tenants pay higher rents will free up funds to build 150,000 affordable homes over the next four years, 30% higher than the previous four.

Under Part L 2010, the proposed residential energy efficiency improvement is broadly in line with that required to achieve a Code for Sustainable Homes level three. Experience shows this is generally achievable through good passive solar design or passive design with renewable energy systems.

Part L1A 2010 aims to reduce CO2 emissions by 25% from 2006.

The cost model is based on a new-build scheme of 6 two bed and 4 three-bedroom houses. The 2 bed homes have a floor area of 78m2 and the three bed homes 88m2. The buildings comply with code level three, are of timber frame construction with an insitu reinforced concrete ground slab, facing brick external walls and concrete tiles on timber roof trusses. The softwood doors and windows are painted and internal subdivision is by loadbearing timber stud partition. Features for the Lifetime Homes standard, National Housing Federation Standards and Housing Quality Indicators are included.

05 / small industrial units

Last year the value of industrial building work in Great Britain was 55% of its 2006 high of £6bn, in real terms. However, the middle of 2010 saw what may be the start of a renaissance of industrial building.

The latest GDP figures show that manufacturing made the largest contribution to growth, with output rising 1% in the third quarter following a 1.6% increase in the second quarter. Experian Business Strategies forecast real-term growth of 5% and 7% for industrial construction in 2011 and 2012 respectively in response to the recovery of exports.

Steel prices, which have since fallen back, began to increase in the first quarter 2010 and rose sharply in the second quarter in response to much higher input costs. Material prices rose 30%, adding more than £200/tonne, which manufacturers were largely able to pass on to consumers.

As a result, the erected cost of simple steel portal frames rose 30% in the first half of 2010 and more complicated industrial building steelwork rose between 22% and 23%.

Under Part L 2010 warehouses will be obliged to achieve a carbon reduction of 34% against their previous standard (see the table on page 51), compared with the average of 25% for all building types. Efficient lighting systems and optimum rooflight design are the areas most likely to achieve the necessary reduction.

The industrial unit model has an insitu reinforced concrete ground-bearing slab, steel portal frame with reinforced concrete pads, aluminium built-up cladding system to roof and walls and internal blockwork walls. Each unit has a separate entrance door and one loading door. Internally the model includes for a small WC block, basic lighting and natural ventilation.

06 / location factors

Rates shown in the models are based on projects built in the South-east and can be adjusted using this table

Downloads

Primary school classroom extension cost model

Other, Size 1.14 mbAffordable homes cost model

Other, Size 1.03 mbIndustrial unit cost model

Other, Size 1.37 mb

No comments yet