The rapidly expanding use of CLT saw its trajectory arrested in the UK by new regulations in the wake of Grenfell, but if safe solutions can be found then the material offers considerable cost and climate advantages over more traditional frame solutions. Alinea breaks down the costs

01 / Introduction

This decade will be remembered by practitioners in the built environment as the moment when mass timber broke into the mainstream of high-rise construction. Standout projects have been constructed recently, suggesting that some cultural and code obstacles are being overcome. Industry and government entities in the US have signalled their commitment to increasing the use of mass timber in construction, with changes to its International Building Code in 2019 permitting mass timber construction up to 270ft (just over 80m). Canada is also making changes to its building code, opening up new opportunities for taller wood designs, while in France, plans for a sustainability law will mean that all new public buildings will be built from 50% timber or other bio-based materials, as part of President Macron’s drive for the country to be carbon-neutral by 2050.

But while timber is becoming more common as a structural building material, the pace of development varies from country to country, and the UK is not among the fastest. Environmental credentials are an obvious reason behind the material’s popularity, but that alone is not enough to ensure its uptake – competitiveness, competence and safety are essential.

A milestone was reached in March 2019, when the 18-storey, mixed-use Mjøstårnet building was completed in Brumunddal, Norway. At 85.4m it is the world’s tallest timber building, according to the Council on Tall Buildings and Urban Habitat (CTBUH), comprising a glulam frame, CLT core walls, timber composite floors and CLT balconies. There are good reasons why it is difficult to imagine such a predominantly timber building being constructed in the UK any time soon, but it does raise the question: notwithstanding what Grenfell has revealed about our design, construction and regulatory processes, why can’t we make more use of the most sustainable material available to us?

A narrower focus: CLT in residential buildings

With the accelerating consciousness of climate change and a growing appreciation from the real estate industry that we must act now to lower our carbon footprint, it would seem a shame to totally discount timber, and particularly cross-laminated timber (CLT), as a vehicle to help deliver more sustainable buildings, especially in the medium-rise residential sector.

That is certainly not to ignore current legislative developments and guidance as a result of the Grenfell tragedy, but perhaps in time, when robust testing has been undertaken and solid case histories have been evidenced, CLT could resume its trajectory towards mainstream acceptance for appropriate building typologies in the UK.

This article is designed to act as a reminder of the known benefits, while examining in more granular detail the areas of cost where opinions might in the past have been mistaken due to an absence of hard commercial data.

02 / Background to CLT

CLT was developed in Austria in the early 1990s and found rapid traction in Germany, Austria and Switzerland, where carpentry and heavier timber construction is very much the norm and a respected, time-honoured building method. CLT was first introduced to the UK through the architect community in the early 2000s, and the seminal Murray Grove – a nine-storey residential block in Hackney by Waugh Thistleton Architects – was completed in 2009. This was an attention-grabbing moment for timber construction as it demonstrated a direct, viable alternative to concrete in higher-rise construction.

The next decade saw a large number of higher-rise CLT structures built, the largest of which was Dalston Works, again designed by Waugh Thistleton, a 10-storey residential structure completed in 2018. An increasing number of public and private sector projects have also been delivered using CLT.

The growth trajectory of CLT for the higher-density residential market sector changed in December 2018 when the new legislation post-Grenfell determined that no combustible material should be present in the outer cavity of “accommodation” buildings over 18m tall. The higher-rise CLT buildings built before that date, such as those mentioned above, all had an external superstructure of CLT. The new legislation did not explicitly ban the use of CLT, but in practice it did have very much this effect. Those pushing for the wider use of CLT see this blanket default restriction as having blocked the opportunity to take advantage of the material’s strengths: short build times, low carbon, passively energy-efficient, low social impact.

The government put out a further consultation paper for review with a closing date of 25 May this year, which presented options for further height reductions and a scope encompassing buildings beyond “accommodation” (ie non-residential). Some are suggesting that through these recommended further limitations on the use of combustible materials the regulators are removing timber and CLT as one of the few sustainable solutions to the housing shortage. As yet no outcome has been stated from this most recent review.

CLT and fire safety: an expert’s view

Can CLT buildings perform adequately in fire? There are fundamentally two possible answers:

- Yes, because CLT chars when exposed to fire so it is inherently safe.

- No, because CLT burns and so is inherently unsafe.

Both are commonly expressed – and the truth lies somewhere in between.

What is relatively easy to agree on is that taking a standard approach to fire safety design for CLT construction is unwise. Standard guidance is inherently applicable only to standard buildings.

It is therefore worth considering what “standard” means. It is generally accepted a typical low- to mid-rise block of one- and two-bed flats is relatively standard, so adopting standard guidance could enable an adequate level of safety to be achieved. But if that same building is constructed in CLT, meaning that the structure itself is a potential source of fuel, the building may then begin to look a bit less standard.

Perhaps the CLT could be encapsulated: overboarded and removed as a fuel source. Would the building then become standard again? That would depend on how confidently one can specify the encapsulation solution. Has it been tested when affixed to CLT? Is there access to test data that shows the encapsulation will not fall off? Who will underwrite the performance and, more fundamentally, what even is the required performance? Similar questions apply to the specification of fire-stopping solutions and, from experience, none of these questions have a straightforward answer. Many manufacturers cannot or will not provide adequate evidence to demonstrate that their products can perform adequately in this arrangement when affixed to or embedded in CLT.

As experience and understanding of the fire safety design of CLT buildings grows, the more it is appreciated that there is nothing standard about CLT in terms of fire safety. However, that does not mean we cannot approach CLT fire safety design a standard way.

BS 7974, for example, provides a framework for approaching performance-based fire safety design. It recommends that the designer:

- Explicitly defines fire safety objectives and performance criteria

- Analyses the proposed design(s)

- Compares the results of the analyses against the defined performance objectives.

This approach differs from that presented in standard guidance, as objectives are explicit. Within standard guidance documents such as Approved Document B, BS 9999 and BS 9991 there are implicit assumptions on the acceptable level of safety. The guidance enables designers to adopt predefined solutions, the use of which is generally accepted to achieve the assumed adequate level of safety without assessment against explicit goals.

Many fire safety objectives for CLT buildings will align with those for standard buildings, for example “to enable safe means of escape within an adequate period” or “to maintain structural stability for a reasonable period”. However, the performance criteria against which these objectives are measured will be more explicit, for example:

- Mitigate the risk of the CLT becoming involved in a fire

- Mitigate the risk of perpetual burning where CLT elements are exposed ie design for self-extinction

- Mitigate the risk of external fire spread as extra combustion occurs outside windows

- Ensure the residual structural section can support the loads both during and beyond a fire.

This type of approach not only allows the designer to adopt current best practice and apply findings from the most up-to-date research, but also allows them to challenge their understanding of the fundamentals of fire dynamics. It forces objectives to be explicit rather than implicit. It requires designers to demonstrate performance rather than assume performance.

One, perhaps daunting, requirement of taking this type of approach is that we must document our knowledge and, more importantly, our assumptions. Do we really understand the mechanisms of self-extinction? Do we understand the rate at which char forms under different types of fire exposure? Can we define what proportion of fuel combusts within a compartment and what externally?

At present, no designer can say categorically they know the answers to these questions. However, that does not mean we cannot develop designs to address these risks. In fact, we are significantly better placed to develop designs that can sufficiently address these risks if the risks are first identified.

So, can CLT buildings perform adequately in fire? The answer is still both yes and no. Only when the design approach adopted adequately and explicitly considers the fundamental risks can CLT buildings be demonstrable as safe.

By OFR Consultants

03 / Overview of the CLT market

For a building product to become mainstream, it probably needs to exhibit a number of key attributes:

- An abundance of stable, low-cost raw material

- Scalable manufacturing capacity

- Efficient supply channels

- Compliance and accreditation

- A legacy of successful proven case histories

- A knowledgeable, informed specification community

- Evidenced carbon footprint reduction

- A solution for future-proofing the building asset.

CLT performs well against these criteria and is on a global trajectory to become a mainstream building solution. The challenge in the UK is to satisfactorily address developing guidance and regulations, as well as understandable perceptions post-Grenfell.

Supply is not the issue: there is 160 billion m3 of standing fibre (trees) in Europe and Russia alone that feeds the structural timber market, and this is growing at 18m3 per hectare each year. Sustainability is not the issue either: every tonne of CLT locks in 1.6 tonnes of C02 while Portland cement generates about 870kg of CO2 emissions per tonne of cement produced and for steel it is 1.75 tonnes of C02 for every tonne produced.

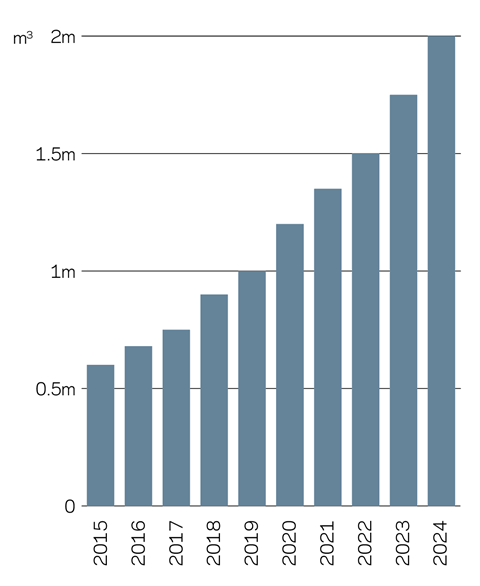

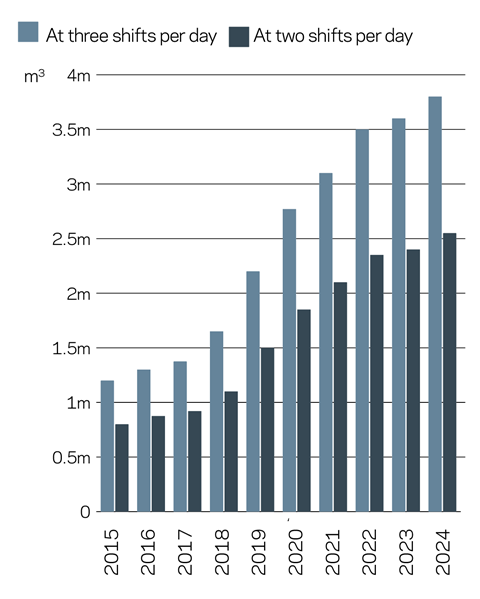

These credentials, together with a cost base that has improved and is better understood, have encouraged expansion. Since 2015 CLT consumption has increased by on average 15% a year, with over 50 installations in Europe alone. Theoretical capacity at three shifts per day on 250 manufacturing days per year will realise annual capacity of 3.5 million m3. Investment in CLT manufacturing technology is at an all-time high. UK consumption has shot from zero in 2000 to 70,000m3 in 2020, which for a principal structural fabric building material is highly unusual, and despite the current height legislation it is still on a path to exceed 100,000m3 a year by 2025.

Outside the UK, building codes are embracing CLT and mass timber, with increasing numbers of CLT framed buildings (at increasing heights) being built. This is a trend that looks set to continue, supported by governments in some locations – political backing which understands that investors and other stakeholders must seriously consider future-proofing their assets against the climate change agenda and the socially aware Generation Z demographic that will comprise a large proportion of future occupants.

04 / CLT versus traditional reinforced concrete frame

The CLT frame building on which the cost model is based has also been designed, priced and market tested with the alternative option of a traditional reinforced concrete frame – which is the predominant solution for the residential market at this height based on a range of factors, with cost being the principal driver.

CLT has long been considered cost-neutral compared with concrete framed alternatives, with its sustainable credentials and programme benefits tending in most cases not to outweigh the supply chain issues and familiarity/surety of concrete in client and design team decision-making. This unfamiliarity manifests itself as a risk for those who have not used CLT before.

Our findings, however, when taking CLT as an alternative framing method to concrete for mid-rise residential, show that there are savings to be made even in a non-optimised scenario, with further benefits of programme and area improvements to be had.

The table below sets out the key elemental variances between a CLT and a concrete option for a typical residential block of up to seven stories (see “About the cost model” for the key design assumptions that underpin these figures).

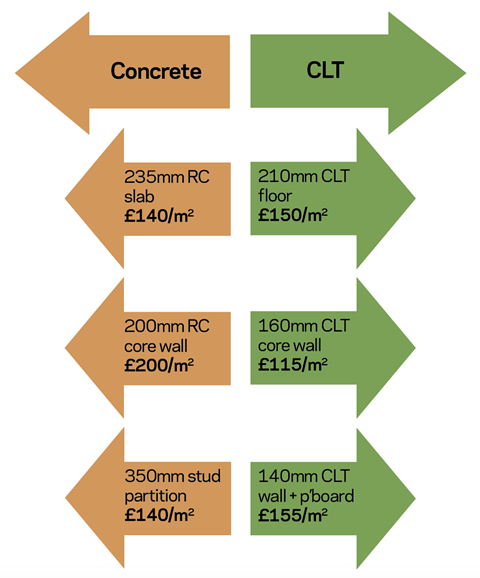

It is important to understand the elemental comparison between CLT and concrete to appreciate which areas of design can glean the greatest savings and also where a hybrid solution could be effective. Obtaining the granularity of information from the supply chain as you would in steel or concrete markets is necessary in order to do this without falling back on the high‑level studies of the past. Key item comparisons between concrete and CLT on a test building are highlighted in the diagram below.

Not all individual components are cheaper than concrete, which reinforces the message that a full appreciation of CLT design and the consequential elemental savings is required to provide a robust cost comparison. Assuming a standard level of existing ground constraints and with an efficient CLT design of up to eight storeys, savings of 3%-7% over a concrete frame residential building could be achievable.

While current fire regulations preclude the use of a CLT substrate to the facade, eroding the programme benefits that would give, overall time savings worthy of consideration remain (10%-15% over a concrete frame). Further opportunities exist around the acoustic performance of the internal CLT walls versus stud partitioning, which – depending on the project specific criteria – could result in additional NIA being generated or a reduction in the GIA. Indicatively this is in the 3%-5% range on a scheme of 200 units or more.

Table: Cost variances between CLT and reinforced concrete for key elements in a residential block of up to seven storeys

| Package | CLT vs RC | Reason |

|---|---|---|

| Substructure |

-20% to -30% | Lighter structure leads to lesser loads on foundations: * Reduced number of piles (by 20%-40%) * Potential to revert to raft foundation Savings predicated on suitable existing ground conditions |

| Frame |

-5% to -10% | * CLT core vs RC core the largest saving within frame; 30%-40% (excl fire protection) * CLT walls/structure more costly than a blade column solution by approx 20%-25% * But these costs offset by subsequent savings in internal partitions |

| Upper floors |

+10% to +15% | * CLT 210mm floors slightly more costly than a 235mm RC slab by approx 5%-10% * Majority of cost increase relates to a requirement for a transfer floor (400mm-500mm) which is extra over a standard 235mm RC slab in the traditional case |

| Internal walls |

-25% to -35% | * Saving relates to omission of standard stud partitions to corridor and demise walls (circa 250mm-400mm); replaced with CLT 140mm walls (captured in frame as noted above) with two layers of 15mm plasterboard each side for fire protection and acoustics |

| Preliminaries |

-10% to -20% | Programme saving of approx 10%-15% leads to the following capital cost reductions: * Saving on all weekly preliminaries cost, management, site facilities, security, consumables etc (about 40%-50% of overall saving) * Specific saving on frame package manager(s); duty and cost picked up in CLT figures (approx 5%-10% of overall saving) * Saving on craneage as mobile cranes priced within CLT install rates (approx 40%-55% of overall saving |

| Overall | -3% to -7% | To achieve a higher level of savings the following can be looked at: * Optimisation of CLT panel sizes/types (potential to save 5%-10% of CLT costs) * Review of critical path fit-out trades and further programme/preliminaries savings |

05 / About the cost model

The cost model is based on a standalone, seven-storey plus half-basement new-build built-to rent residential building in outer London, housing 251 apartments and associated amenity spaces, car parking and retail units.

The shell includes a piled foundation with in-situ concrete lower and upper ground floor slabs; an in-situ concrete transfer slab to level 1; CLT upper floor and roof slabs; CLT core with PCC stairs and CLT frame consisting of 140mm wall sections.

For the purpose of aligning with current Building Regulations Part B we have assumed the facade comprises a Metsec steel frame system substrate with Rockwool insulation and a hand-laid brick skin. This is code-compliant in respect of fire regulations while also going back-to-back with the traditional concrete preferred route of hand-laid brickwork as part of a punched-hole window solution. For compliance with anticipated future legislation, the model assumes there are no exposed areas of CLT such as in apartments and lift cores. Internal plasterboard has been allowed where previously these areas could have been left exposed and treated for spread of flame. Sprinklers are provided to all apartments and landlord areas. Three 15-person lifts at 1.6m/s serve all floors and include one with firefighting control.

The apartment fit-out ranges allow for wall, floor and ceiling finishes, timber batten floors where appropriate, and fixed furniture and fittings. Retail units are taken as grey shell so include shop-front glazing and doors but exclude all fit-out (by tenant), allowing for capped services only.

All rates are base date Q3 2020. CLT supply rates assume euro exchange rate of 0.91. Exclusions from the model include fees, VAT, demolitions, site clearance, external works, incoming utilities, section 106/278 contributions, CIL payments and the like.

Key metrics:

- Total GIA: 27,511m²

- Residential GIA: 22,631m²

- Residential NIA: 14,759m² (plus amenity 871m²)

- Number of units: 251

- Other uses: undercroft car park 3,348m² (with 101 spaces); retail 1,532m².

Acknowledgments

This article was written by Alex Hyams and Steve Watts of Alinea, James Sweet of Engineered Wood Solutions and Dr Kate Swinburne of OFR Consultants

Download the cost model using the link below

Downloads

CLT frame cost model

PDF, Size 58.53 kb

No comments yet