It turns out that the construction industry is using substantially less ‘stuff’ than it was 15 years ago. Is this a blip or a victory for resource-efficiency?

This January, a new phrase entered the already endless sustainability lexicon. It came, oddly enough, from the mouth of an executive at Swedish furniture giant Ikea. “If we look on a global basis, in the West we have probably hit ‘peak stuff’,” said Steve Howard, the firm’s head of sustainability at a Guardian newspaper-organised debate. “We talk about peak oil. I’d say we’ve hit peak red meat, peak sugar, peak stuff … peak home furnishings.”

An interesting idea, you might think – but possibly not the most authoritative source for a potentially world-changing concept. However, right on cue, came official data in February showing that Howard’s phrase was not just a marketeer’s patter, and that the UK’s consumption of natural resources has actually been steadily dropping since the turn of the century.

And not by a small amount. In fact, the analysis of a range of government data by the Office of National Statistics (ONS) showed that, excluding fossil fuels, the best estimate of the UK’s global material footprint (that is, including imports and exports as well as just domestic materials) fell by almost exactly a third between 2001 and 2013, to 6.4 tonnes for every person in the UK (about the weight of a large African elephant). Yes, the period included a huge recession, but over the 12 years as a whole the economy actually grew, meaning the amount of economic activity generated per unit of materials – known as “resource productivity” – shot up an enormous 59.4%.

This trend is interesting for the construction industry, because a large part of material use comes from construction: the 250 million-odd tonnes of aggregates and other mineral products make up by far the largest single material flow in the economy. In a finite world, reducing the sector’s reliance on precious and often irreplaceable materials would be a huge cause for celebration. It could also have huge implications for measuring the sector’s progress on sustainability and its likely ability to continue to improve to meet the Construction 2025 targets.

It may be difficult to draw firm conclusions from such broad-ranging data, but Building has obtained detailed breakdowns of the data behind the ONS figures, which do allow some pretty strong verdicts to be drawn. Peak stuff, it seems, works for construction too, with sharply declining material use since the millennium. So what is going on here, what exactly does the data say, and where is the industry’s use of materials likely to go in the future?

A less material world

The ONS’s numbers are based on the British Geological Survey, plus information from HM Revenue and Customs on imports and exports. While it does not record construction materials specifically as a category, it does include categories of materials which are clearly predominantly used for construction, such as sand and gravel; slate; limestone and gypsum; and marble, granite and sandstone. The data also includes other categories, such as timber and iron products (such as steel), where construction will be a major but by no means exclusive user of the materials.

When you get back to growth, often materials demand just never catches up

Jerry McLaughlin, Mineral Products Association

The volumes of these materials used seems to reflect the general trend. In total, the ONS figures for construction-related categories show that the amount used has fallen by 35%, from 298 million tonnes in 2000, to 193 million tonnes in 2013, the latest year for which it has data. This is a greater fall than that of materials in the general economy as a whole. Of all the products recorded, only timber has seen its use rise, while recorded use of iron-based products has more than halved.

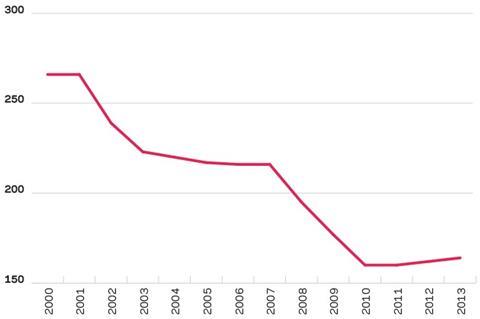

Of course the recession in construction was far deeper than that of the economy as a whole, so could this shift just be a reflection of less building work happening? Not so, it appears. When plotted against inflation-adjusted construction output, the trend is actually even more pronounced. Where in 2000, 266kg of materials were used for every £100 spent on a building site, by 2013 that had fallen to just 164kg. That’s a massive 38% shift.

While the concept of “peak stuff” might be new to many of us, one body that shows no surprise at this information is the Mineral Products Association (MPA), the trade body for producers of aggregates, cement and similar materials. Its members produce the vast bulk of construction materials in the UK, dwarfing the weight of structural steel traded by a factor of 50. Jerry McLaughlin, director of economics and public affairs at the body, says: “This is an issue that’s very close to us. Historically, the supply of these materials actually peaked in the boom of the late 1980s before the recession. Typically what happens in a recession is you get a bigger fall in construction output than the wider economy, and you get an even bigger decline in minerals use than in construction output. When you get back to growth, often materials demand just never catches up.”

The MPA captures data for the whole industry based on UK sales, rather than the extraction, imports and exports information which the ONS relied upon. This information paints a very similar picture to the ONS figures. Since 1997, it finds, sales have fallen from 268 million tonnes, to 219 million tonnes in 2015. That means the 248kg of minerals used for every £100 of construction in 1997 fell to 167kg by last year.

The age of efficiency

The most obvious next question is how this change has occurred. There seems to be relatively little clear evidence, but experts suggest many factors come in to play. “It’s difficult to quantify exactly why this is happening,” says McLaughlin, “but clearly over time people are using materials more efficiently, with the recessions helping to drive that, and clients demanding more efficiencies in design.”

This economic driver of reduced material use can be seen in major projects such as the M25 road-widening scheme and the Shard, where engineers attempted to strip out surplus structural steel, according to Balfour Beatty’s head of sustainability Paul Toyne, who worked on the project while at Shard engineer WSP. “On the M25 we changed the design of retaining wall sheets so that 30-40% less steel was required, resulting in both a material cost saving and quicker installation.”

On the shard we worked hard to think how we could strip out structural steel while keeping the necessary structural strength

Paul Toyne, Balfour Beatty

There has also been the drive to greater recycling, both in terms of demolition and construction site waste, and in terms of the make-up of “new” construction materials. According to figures from Defra, of the 45 million tonnes of site waste generated by construction and demolition each year, 87% is now recycled – way above the UK’s 2020 target of 70%. Much of this activity has been driven by the growing expense of putting materials in to landfill. Balfour Beatty’s Toyne says: “Balfour Beatty has had an increase in recycling rates on our sites. Typically, we are now diverting 94-95% of construction waste away from landfill. The challenge now is about how to retain the value of that material in our supply chain through reuse.”

Often this site waste is reprocessed into a form that can become fresh construction materials. Structural steelwork has always been re-used where possible, but the grinding down of concrete into aggregate for fresh concrete, foundations or landscaping is an example of how materials are being recycled that weren’t previously regarded as high enough value to recover. For example, Toyne says that material dug up during Balfour Beatty’s M25 widening job was ground down on site and re-used in the landscaping works such as banks for noise attenuation, or bunds for water management. According to the sustainable concrete forum, 28% of aggregates used in 2014 by the industry were from recycled sources.

It’s not just the recycled content of materials that may be reducing the industry’s resource use, but also the improved performance of newly developed materials. Steve Crompton, national technical director at Cemex UK, says the last 5-10 years has seen an acceleration in the development of higher strength concretes, which means that smaller columns and beams can provide the same amount of structural support as previously. Post-tensioned concrete can, similarly, reach much greater spans. Any reduction in concrete mass then also reduces the weight of a building, decreasing the volume of foundation material required. Likewise, high-tech asphalts mean thinner layers are needed to provide the same performance on new roads.

At the same time as the use of heavy materials has been decreasing, IT and building services have become ever more important. Crompton says: “There’s much more emphasis on services, which has been upping the overall cost of a building and reducing the share spent on materials.”

Graph: kg of construction materials per £100 of construction work

Even less stuff?

Despite this, the question the MPA is currently asking is whether the trend for less resource intensity has actually come to an end. The latest sales data shows mineral use increasing between 2013 and 2015 at a faster rate than the construction economy has been growing – the first time in nearly 30 years this has happened. So far, the assumption is that this is just a hiccup in the general trend, caused, most likely, by a shift toward resource-heavy construction such as roads, and greenfield rather than brownfield housing. “We’d need to have a fairly long run of consistent data before we thought this trend was going to finish,” says McLaughlin.

Certainly, the indicators from the industry are that the innovation driving much of the greater resource efficiency is gaining pace, as the concept of a “circular economy”, where resources are endlessly repurposed, grows. Julia Stegemann, professor of environmental engineering at University College London, says: “The idea of zero waste is not possible in reality. But the circular economy is an ideal that motivates people as a way of thinking.”

Coming out of this concept is the Design for Deconstruction movement, which aims to design buildings by using standardised and discrete components in a way that they can be disassembled and re-used at the end of a building’s life, and which is increasingly influencing designers.

A different strand comes from the research Arup is doing around 3D printing of bespoke metal structural junctions designed specifically to deal with the forces put on them. Used instead of more over-engineered generic designs, this has allowed it to cut the height of junctions in half and the weight by up to 75%. Simon Sturgis, founder of Sturgis Carbon Profiling, says: “If you print a structural beam you can make it to an optimal efficiency to deal with the stresses on it, which is potentially so much more efficient. If you expand that idea, then the potential is to make buildings with far less material.”

These ideas aren’t wholly new, either – it is more than 15 years since architect Andrew Whalley led Grimshaw’s team designing the Eden Project on the basis of “radical resource efficiency”. Inspired by the natural world, the project used such lightweight materials that he was able to claim the air inside the centre’s two biomes weighed more than the structures themselves.

There is one further and much more radical challenge that the concept of “peak stuff” throws at the construction industry, however. For the wider economy, much of the discussion has revolved around the way that the huge advances in digital technology mean that consumers today don’t need as many physical books, DVDs and CDs as they did previously – just one iPhone, laptop and broadband connection. For construction this plays out differently – buildings will always be physical objects. But could it be that the potential for working and shopping from home enabled by digital advances actually reduces the demand to construct new physical shops and offices?

Anna Surgenor, senior sustainability adviser at the UK Green Building Council, thinks it will at least change the pattern of demand. “Our retailer members are already looking at what their future buildings will look like, if indeed they will have them at all. Offices are much more about flexible working, and demand will change.”

Fortunately, Cemex for one isn’t envisaging the industry becoming a casualty of the digital age. Andy Spencer, sustainability director at the firm, says: “With retail, the reality is that if they don’t want a shop they’ll want a warehouse – there’ll still be demand for materials.”

We may be becoming more efficient, but there’s no need for the construction industry to panic about obsolescence just yet …

Less material in the market

The St James’s Market scheme in Piccadilly, central London, being built by Balfour Beatty for the Crown Estate, is just one example of clients and contractors working together to minimise the use of materials on site. The £90m retained-facade job involves the demolition of two existing properties to basement level to create 31,600m2 of office and retail space.

The project involved the retention of the original grade II-listed 1,600-tonne facade, but also focused on reducing embodied carbon through increasing recycled content in key building products and promoting lower carbon concrete. Ultimately it achieved 36% recycled content in building materials, and sent over 98% of waste to recycling rather than landfill. Targeted re-use has resulted in carpet tiles, slates and switchgear being donated to London charities and training colleges, while the contractor is attempting the salvage and reinstallation of 10 tonnes of ornamental lead work.

No comments yet