Tender prices are still falling while material prices and wages are rising, says Peter Fordham of Davis Langdon, an Aecom company. All these bank holidays aren’t helping either

01 / EXECUTIVE SUMMARY

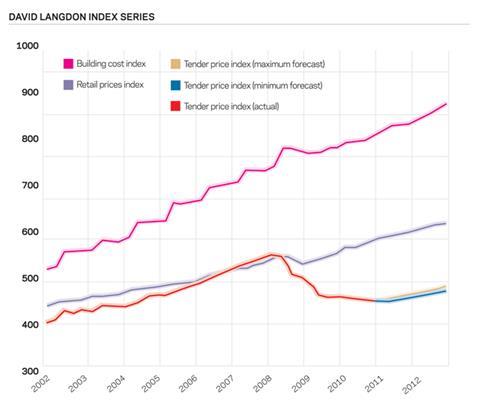

Tender price index

Tender prices are erratic as future workload weakens but input costs rise. Overall tender prices in first quarter 2011 fell slightly again.

A divergent market looks set to open up between London and the rest of the country.

Building cost index

The deflation that occurred in the second half of 2009 has long gone. Building costs have been rising steadily since then despite a continuing pay freeze. Costs rose 3.5% over the last year and are projected to continue to rise by between 3% and 4.5% a year over the next two years.

Retail prices index

In March, general inflation measures eased back from their February highs but, at 4%, the Consumer Prices Index remains at double its target figure. The annualised figure is expected to rise further this year before falling sharply in 2012. Inflation as measured by the Retail Prices Index remains higher, at 5.3%.

02 / TRENDS AND FORECAST

The construction industry in the UK is currently being pulled in different directions. The outlook for many contractors is uncertain: the advent of the new financial year heralds the real start of the government’s public sector cutbacks; the private sector is making more positive sounds but bringing projects to market still seems a long way off. At the same time contractors are faced with another round of soaring input cost rises as global uncertainties and improving demand send commodity prices upwards.

These conflicting signals are resulting in contractors submitting prices that are even more difficult to predict than ever. Some are clearly fearful of their order books in the medium term and taking an even sharper look at the tenders they are submitting. Others are wary of making “suicidal” bids and attempting to reflect the higher prices their own suppliers are demanding. As such some tenders being received seem to be moving upwards while others seem to be taking the trend even lower. This could be a literal (and exaggerated) definition of “bumping along the bottom”.

Although there are clear examples of tenders moving in the opposite direction, Davis Langdon’s average tender price index shows a further fall in the first quarter of 2011 of 0.5%, leaving prices 2.5% lower than a year before. The few substantial projects that are coming to market are keenly fought over but there are also increasing examples of contractors taking a more discerning attitude towards projects to bid for. Even projects that were being keenly hunted six months ago have found difficulty in compiling a tender list of first choice contractors.

Groundworks, concrete and piling tenders remain extremely keen for the most part. Steelwork tenders remain competitive as capacity remains seriously under-utilisied, in spite of manufacturers materials costs increases imposed at the start of the year; and some mechanical and electrical services prices have risen, in large part due to material price movements - notably copper. At the same time, overheads and profit allowances in some cases may be creeping up, if only to try to maximise the value of post-tender variations: 3.5% to 4.5% is now more common again although examples of less than 1% can still be offered. Preliminaries allowances remain reduced and often as single figure percentages. It is quite clear that some contractors are submitting below cost tenders in the hope of recouping money down the line from client changes and their subcontract partners. Employer contract amendments may often be resisted at tender stage but objections tend to melt away if contract success becomes dependent on it.

Main contractors are aware of the changes coming in the mix of construction work likely to be available over the next few years and endeavouring to reposition themselves in areas where they may not historically have been strong. This includes trying to break into the non-traditional sectors of energy, waste and infrastructure where future opportunities should be brighter. Similarly contractors are continuing to move down to lower sized projects than they might once have considered.

There are very clear signs of activity in the London development market with a number of developers re-activating dormant sites and moving ahead with schemes that aim to complete in 2012 or 2013, to meet the anticipated demand for new space that will by then be required. Elsewhere, however, there is still very little sign of real activity. Enquiries have picked up, building clients are re-examining the feasibility of schemes and progressing work to planning stage. But funding remains a real issue. Pre-lets remain mandatory even though supply shortages are beginning to become apparent in some areas and office rents in some parts of the North and Midlands have begun to rise. Credit availability actually seems to be worsening, with lenders to the commercial real estate sector blaming refinancing requirements and uncertainty over future prices as constraints on availability. Last week’s report on the banks requiring them to increase their capital reserves may cause them to retrench further. As a result, some contractors are actively trying to generate work by offering funding to “pump prime” schemes.

Forecasts from the Office for Budget Responsibility released at the time of last month’s Budget downgraded its forecasts for GDP growth over the next two years to 1.7% this year and 2.5% next year. These figures are weaker than the long term trend but business investment intentions are strong. Some independent forecasters think these figures are too optimistic but the International Monetary Fund issued very similar numbers for the UK last week.

Last month’s “Budget for Growth” revealed some initiatives that may help the construction industry. Housebuilding in particular was encouraged with the £250m FirstBuy scheme to assist first time buyers who have been unable to obtain mortgages and the announcement of the release of public land such as MoD sites for housebuilding, for free until the homes are sold. Residential development should also be encouraged by the reform of stamp duty and the rules for Real Estate Investment Trusts and, following consultation, the relaxation of planning rules to facilitate the conversion of vacant office and industrial space to residential use. Housebuilders’ share prices rose immediately after the Budget announcements but some have since fallen back.

The country may be embarking on a slow recovery but the construction industry is likely to fall back into recession as the public sector cutbacks impact quickly on 2011 workloads. Contractors are faced with rising input costs while trying to secure workload for declining order books, leading to potential difficulties for those firms that undercut their cost base too severely. Construction work on the London Olympics is now winding down but prospects for the London construction industry are looking stronger by the day. Office development starts are going ahead and residential construction is active, both at the luxury and more common ends of the spectrum. The first quarter has seen some keen prices in the London market but as more work is brought to site and the major contractors and subcontractors secure a portion of workload, prices may begin to harden. Elsewhere prices seem likely to remain cut-throat for some time to come.

Over the next 12 months, tender prices are expected to rise in the London area by 2%-3% but elsewhere prices may have further to fall and price movement between -1% and +1% should be expected. The following year could be even tougher for contractors if the forecasts of commentators such as the Construction Products Association and Hewes and Associates prove correct. However, in London, activity should continue to strengthen, resulting in further price rises as contractors attempt to restore some margin: price rises of 3%-4% may occur but elsewhere contractors will still struggle to make a profit and prices may not increase at all.

03 / ACTIVITY INDICATORS

Construction output

Teething problems continue to beset the Office for National Statistics (ONS) since its takeover of the compilation of construction output and contractors’ new orders statistics from the Department for Business, Enterprise and Regulatory Reform. Its latest issue centres on the construction output figures published in February. It turns out that the value of work undertaken in 2010 in the public and private housing and infrastructure sectors was much higher than the figures published in February suggested. Public housing work was 33% up at £4,774m, private housing work 18% more at £1,1965m and infrastructure 14% higher at £12,541m.

The latest figures suggest that the value of output in Great Britain last year was almost 10% higher than in 2009 and in constant prices was 14% higher, just 3% down on the record year of 2007.

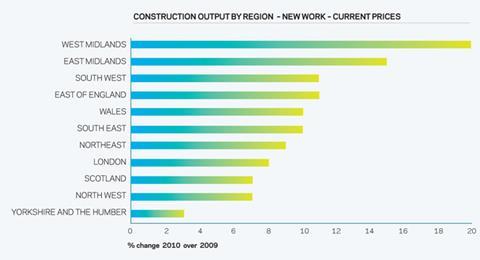

In current price terms, the statistics show that every region benefited from an increase in output last year, however, understandably, some benefited more than others.

The Midlands were the largest beneficiaries from an increase in workload. The West Midlands particularly, saw a massive increase in public sector workload, both housing and non-housing related.

The increase in workload in the East Midlands was more evenly spread but housing, both public and private, was the biggest growth sector.

Yorkshire and Humberside’s construction industry saw the weakest growth: it benefited from a 40%+ increase in public sector work but private sector activity,

industrial and commercial, fell away.

Nationally, activity peaked in August last year and the statistics suggest that output since November has been noticeably weaker with a fairly even drop across all sectors. However, if anything, public sector work has fallen slightly less than the private sector.

Contractors’ new orders

The volume of new orders obtained by contractors in the fourth quarter last year, as measured by ONS, displayed an unexpected, and surprising, rise. The figures show that the volume of orders (at constant prices) leapt by 18% compared with the previous quarter, representing the highest level since the third quarter 2008. Even more surprisingly, the figures show an increase across every sector with new orders for public non-housing work leading the way - this represents a bounce back to the level of new orders being placed in the market at the end of 2009 and beginning of 2010 when contracts were being pushed through ahead of the general election. Regrettably, the increase in orders for new private commercial and housing work that had occurred in the third quarter was unable to be maintained and the fourth quarter figures were, in reality, virtually level.

The relatively buoyant picture painted by the ONS statistics do not ring true for many in the industry but the figures are supported by Markit’s monthly construction purchasing managers’ index. Except for December, when a poor month was blamed on the severe weather, the index has reported 13 consecutive months of growth in activity and, similarly, new business received by UK construction companies increased for a 13th successive month in March.

However, Markit’s survey points out that confidence among contractors is at a three month low with companies wary about the impacts from public spending

cuts to come. These concerns are echoed in the forecasts of future construction output by industry commentators. The latest figures from the Construction Products Association see three years ahead of slight overall new work output declines from 2010’s strong showing with growth not re-appearing until 2014. Latest figures from Experian are more bullish, forecasting a bounce back in 2013 but forecasts by Hewes and Associates are even more pessimistic than the CPA, expecting a big dip in output in 2012 with the private sector failing to fill the gap left by a drastic reduction in public sector work.

Education and communities and local government spending is being curtailed over the next three years, ensuring a reduction in project starts in these sectors in 2011.

04 / BUILDING COST INDEX

The Building Cost Index, the notional measure of the cost of construction materials and national wage agreement building labour, has pushed higher, registering a rise of 3.5% over the year to the first quarter 2011, despite a continuing wage freeze for building and civil engineering operatives. It seems likely that at least this level of inflation will persist over the next two years.

Labour

Wage rates for building and civil engineering operatives employed under the Construction Industry Joint Council (CIJC) Working Rule Agreement have been frozen since June 2008. The normal anniversary date for wage revisions is the end of June and talks are expected to begin shortly between employers and unions to determine any changes to pay and conditions that can be agreed.

The Building and Allied Trades Joint Industrial Council has already reached an agreement for its members, generally the Federation of Master Builders and their employees, for 2011. They secured a 2% wage increase last September that was supposed to apply only until 12 June 2011 but the new agreement reached last month only comes into effect from 12 September this year, providing just a 1% increase to the main rates of pay. The agreement was reached in recognition of a bleak outlook for the industry and, in consequence, the non-deliverability of any higher rate of increase. Will this set the pace for the larger group of workers under the CIJC? The unions’ side will be aware that self-employed labour rates are still falling and contractors have been reducing staffing levels continuously for the last nine months.

Even without wage increases the cost of employing people is rising. In April there was the 1% rise in National Insurance contributions payable by employers, although this was mitigated for lower paid workers by an increase in the threshold before which NI is payable. At the same time, employers will have to fund the two extra bank holidays due to all staff, the first for the Royal Wedding on 29 April and the second for the Queen’s Diamond Jubilee in June 2012.

Materials

The uptick in input costs faced by contractors has been because of the rise in materials costs prices, led in particular by commodities. Figures for construction materials prices produced by the Office for National Statistics show that the increase over the year to February surged back to 9.2%. The average over the last 12 months has been 7.7% indicating the inflated level of price increase faced by contractors over a considerable period of time.

A new steel price spike has been the cause of prices rising early in 2011 on top of the jump that happened last summer. ONS figures show that fabricated steel prices have risen by 27.5% over the year to February and reinforcement prices by 23.7% over the same period. The causes behind the latest rise in prices were examined in some detail in a previous article in Building (Specialist Costs: Steel and Concrete, 18 March, page 50) but were largely due to a simultaneous rise in the price of iron ore, coking coal and scrap, the principal ingredients in the manufacture of steel. This caused Tata to raise its prices for structural steel sections by £50 a tonne in January, followed by a further £95 a tonne in March, a rise of about 17% on basis prices.

The pressure on steel raw materials prices has now subdued. The Australian floods in January caused a sharp rise in the price of coking coal as the world’s principal supply was disrupted. Contract prices for the April to June quarter have been settled at about $330/t (£229), 45% higher than in the first quarter but spot prices are now falling. Supply disruption caused by the floods is expected to last until June but then coal prices are expected to return to a pre-flood level of about $225-250/t (£156-173). Iron ore prices rose steadily by about 50% from the middle of 2010 until mid-February, resulting in record contract prices being established for second quarter deliveries. Part of the rise in iron ore prices had arisen because of India’s banning of exports from Karnataka province, which has now been lifted. Spot iron ore prices fell quite sharply between mid-February and mid-March. The Japanese earthquake and tsunami has hit steel production in Japan, the world’s second largest steel producer after China, reducing demand for both coking coal and iron ore. In the medium term, however, demand should rise as reconstruction commences. Iron ore prices are now rising again as Chinese steel mills begin replenishing stockpiles, in part in anticipation of increased steel exports to Japan.

Although European steel prices rose 20% in the first six weeks of 2011 in response to the raw material price increases, subdued demand has meant that prices have remained steady for the last two months. Steel prices are currently trending lower on the London Metal Exchange and cash and futures prices fell 6% in the first week of April but 15-month prices remain 14% higher than current cash prices.

No comments yet