Technically the construction industry is in a recession, but many firms continue to report stable activity levels for now, says Michael Hubbard of Aecom

01 / Executive summary

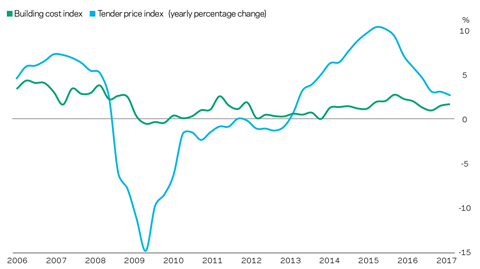

Tender price index ▲

The rate of annual increase in tender prices increased by 3% in Q4 2017. This yearly rate of change is proving resilient against a backdrop of falling industry output.

Building cost index ▲

A composite measure of building input costs maintained an elevated trend of broadly 2% in Q4 2017. Foreign exchange-induced inflation continued to push materials costs higher.

Consumer prices index ▲

The annual rate of change was 3% in December. The yearly rate of change fell slightly for the first time in six months but remains above its target.

02 / Trends and forecasts

Even a new year brings with it old industry issues. Carillion’s story is a salutary reminder of the structural issues that dog the industry. Two questions arise in the immediate aftermath: whether this is just the first domino to fall in a series; and whether this disaster might herald changes to the common operational practices of the industry. If it does lead to fundamental industry changes over the longer term, or if legislation is introduced to implement the lessons learned, could this signal the beginning of the end for current contracting business models?

Vertical and horizontal industry disruption is a guaranteed outcome of the fall of this industry behemoth. The probability of the situation leading to an immediate systemic industry or economic crisis is low, but it will lead to individual crises for smaller firms in the supply chain. Some sectors and regions will experience greater volatility because of Carillion’s sector and geographic footprint. Other sectors, where the firm had less presence, may escape more or less unscathed.

The number of affected firms will become clearer in coming months, with the cumulative effect of these smaller firms suffering or collapsing having implications for the industry’s capacity overall. Neither will the situation do anything to help a sector that sees more insolvencies and liquidations on average than any other UK economic sector. The need for cash flow above all else suggests the precariousness of some business models. In the case of Carillion, the fact that it went straight to liquidation underlines how little value there was left in the company – and how quickly the end arrived.

“Sanity not vanity”, “quality not quantity” – call it what you will. As a slowdown takes hold, some trade contractors are indicating they will double down on a strategy that focuses on margins rather than chasing turnover. The same is said in some principal contractor forums. This strategy involves improving financial performance and supporting margins by maintaining tendered price levels rather than bidding low in order to win work. Selective tendering also plays a part in the overall strategy. This is an attempt to maintain the balance towards a seller’s market, in the face of a weaker outlook and less work over the horizon.

Given the long tail of the construction supply chain, this is a significant development if firms are able to take this commercial route. The market is clearly slowing, and the nature of the supply chain response will indicate how resolute these commitments really are not to chase work at any price. The implications of more supply chain firms scaling back are that capacity is removed from the industry. In doing so, supply and demand norms suggest that price levels should receive support, even against a background of lower work volumes.

A preference to scale back a turnover target in the face of an industry slowdown is plausible – but only where the option to do so exists for a particular firm. Financial strength and the ownership structure of any firm are two factors that might preclude this route. Clearly, commercial attitudes are still influenced by events flowing out of, or relating to, the last industry downturn. It has not been uncommon to read in financial results reporting that “problem jobs” were still trading out over the last few years, adversely affecting financial performance.

These “problem jobs” often result from projects having been tendered at low prices. Poor margins are regularly crystallised from the outset. Profitability then becomes much harder to secure, especially in the face of increasing competitive pressures and where there is growing tension between input costs and output prices. This can play out even when the post-contract period is used to attempt to improve a project’s financial position.

Changing market trends will put a further squeeze on principal contractors. The ability to pass on similar or higher supply chain prices will be stymied by increasingly competitive conditions among this peer group – particularly if clients pursue lower or lowest prices in an easing market.

Contract terms and conditions are likely to see shifting trends in the course of 2018: some terms and conditions will be worked harder in respect of liabilities and clauses that are affected by Brexit issues; and softer contractual positions may be taken in lieu of lowering tender prices in a commercial bid.

With a bumpier economic ride expected ahead for the UK, its gross domestic product figures for Q4 2017 displayed resilience, with a 0.5% quarterly change from Q3 2017. Although this showed the economy holding up overall, consumer confidence and associated spending was weaker than expected. UK consumers are reining in spending – which is one of the central pillars of the UK economy – while consumer borrowing remains high and mortgage approvals are at their lowest in three years.

Manufacturing is supported at present by the lower pound. Confidence among manufacturers is relatively strong, as is capital investment growth in this sector, but the latest business surveys indicate a slight weakening in sentiment. Growth is still growth, though, however it arrives.

Worryingly, the construction sector returned a negative contribution of -1% to the Q4 gross domestic product figures. Rather ingloriously again, construction was the only UK economic sector to contract quarter-on-quarter in this official statistics data release. Nonetheless, the GDP figure for 2017 as a whole was 1.8%, confounding most economic forecasters’ views for 2017. That said, it does mark the slowest growth rate since 2012.

Upside potential in the UK’s outlook relates to the global economy now seeing its broadest upturn in activity since the financial crisis. Further, the EU’s economic growth rate – at 2.5% annual growth – is the strongest recorded since the financial crisis. The UK might then be able to benefit by hanging on the coat-tails of this global pick-up, receiving an economic fillip – particularly in the case of those UK firms that export their goods and services.

UK business investment remains muted, however, because of anxiety for the short term. Although global optimism is found in the International Monetary Fund’s revised economic forecasts, this news from the IMF is tempered by the fact that the UK is the only country in its list not to receive an upgrade to current recorded growth rates. The UK appears to be finely balanced, however, in its sentiment surveys, confidence and recorded growth going into the new – and very probably eventful – year ahead.

03 / Activity indicators

All work construction output increased by 1.6% in Q3 2017 compared with the same quarter in 2016. However, a more recent measure of volume change saw output slip by 2% from the second to the third quarter of 2017. In other words, while output grew over the year, it did so at a slowing rate. The same applies to new work data across the same time frame.

In a telling trend for changes in output, only private housing increased among the various construction sub-sectors in terms of three-month on three-month changes. As in many previous output data releases, the private housing sector led the way once again with its rate of change. However, a growing number of housebuilders are accepting that the peak of recent housing output has been passed.

Positive contributions to newwork were also made by the public housing and infrastructure sectors. Nonetheless, a trend of lower overall industry output is underlined further in these data releases from the Office for National Statistics. Context is vital, and although industry output is slowing, it does so from a position of record highs.

New orders for main contractors posted a 25% increase in Q3 2017 compared with the same period a year earlier. This rebound came after recording a significant fall of 13% in the Q2 2017 figure. The Q3 upturn was driven mainly by infrastructure (+111%), where HS2 contracts were awarded. The Office for National Statistics states that “the 37.4% growth in new orders is the highest on record, exceeding the previous high of 32% seen in Q3 1987, which occurred as a result of new orders placed for the construction of the Channel Tunnel”. Excluding the infrastructure component, new work orders increased by 4%, primarily because of the housing sector.

The lumpiness of infrastructure data recorded in the national statistics masks a more recent survey by the Civil Engineering Contractors Association. Its workload balance survey for the fourth quarter of 2017 declined for the first time in five years, although the balance was -4%. Optimism remains, however, as a higher balance of firms expect workloads to increase over the next 12 months, up to 28% in the fourth quarter from 23% in Q3 2017.

Headline sentiment surveys for the construction industry held up over the final quarter of 2017, with some showing a slight pick-up. Although sentiment was resilient for parts of the industry, this does not interrupt an overall trend to expected lower total output.

The Federation of Master Builders’ State of Trade survey in Q4 2017 reported construction SME workloads slipping marginally, although a healthy survey balance of 35% still indicated rising workloads. New enquiries and expected workloads among SMEs were beginning to move, but the survey balance of firms reporting these trends remained low at 16%. Experian’s Leading Indicator index also signalled an industry that is experiencing respectable activity levels for the time being.

Construction is experiencing a softer patch, yet some support is available from the economic backdrop and corresponding general economic surveys. London is the most pessimistic of the regions reported in ICAEW’s business confidence index survey, the capital being below the UK average in all but one quarter since the EU referendum.

Construction-specific surveys report a similar trend too. According to Experian’s survey, the North-east and Yorkshire lead the way for construction activity, followed by the South-west and the East Midlands. It is not only residential development but a broad base of activity across all construction sectors that underpins this regional buoyancy.

A / Aecom indices

04 / Building costs and prices

Aecom’s tender price index pushed higher by 3% in Q4 2017 compared with the same period in 2016. This is tangible evidence of inflationary pressures still present in the system, supporting the findings of many industry surveys throughout last year in which supply chain firms indicated they were experiencing rising costs and prices. Furthermore, many of the surveys show a continuation of the trends over the short term and beyond. The same underlying inflationary input cost themes are at play, except that it is not now all a one-way pass-through into selling price inflation, as in recent years.

Some respite is felt from the earlier foreign exchange-induced input cost inflation. However, imported inflation is still being sucked into the economic systems of the UK because of the prevailing lower sterling exchange rates. Although sterling is now strengthening against the US dollar, it has not made the same amount of headway against the euro.

A considerable proportion of construction materials used in UK construction are imported from the Eurozone. The impact of euro-denominated cost fluctuations has stabilised somewhat, and there will remain upward pressure on these input costs: firstly, from the current lower rate of sterling against the euro; and, secondly, because it is believed that earlier episodes of foreign exchange-related inflation linger in economic systems for longer. It follows that consumer price inflation is very likely to experience above-average levels of change for an extended period. Likewise, in a construction environment, foreign exchange rates combined with a project’s profile or exposure to imports will be a source of challenge for some time to come.

Concerns around industry labour resources remain. ICAEW’s business confidence survey records construction as the UK industry sector with the highest level of concern for the availability of non-management skills. Construction and the other sectors sharing this anxiety tend to rely on non-UK workers, according to ICAEW’s report. The Federation of Master Builders’ State of Trade survey corroborates this general view, suggesting that the current labour shortages are the worst seen for a decade, with two-thirds of firms struggling to hire key trades on site.

More generally, Experian’s industry survey recorded only a third of firms stating they had no constraints to their work, which is down from half of firms in the middle of 2017. Wages for site staff display synchronicity with output changes. A similar narrative to that for output – higher over the year but rising at a slower rate – applies to an aggregate measure of changes in wage rates for site disciplines. Yearly change is broadly 1.5% to 2%.

Construction sentiment is holding up on the whole, despite the mixed backdrop of economic news. Trade contractors are still mostly confident on workload further out into 2018.However, talk of potential options to navigate a path through expected higher turbulence clearly indicates that they are seeing a hazier picture ahead, which main contractors have seen for longer.

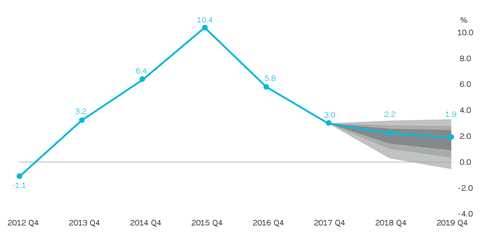

Aecom’s baseline forecasts for tender price inflation are 2.2% from Q4 2017 to Q4 2018, and 1.9% from Q4 2018 to Q4 2019. Although tendering activity is reducing, there is sufficient work expected to maintain positive yearly inflation, when combined with the other inflationary drivers. There is marginal downside risk expected to prices over the coming forecast period, with increasingly more downside risk weighing on the outlook through to Q4 2019. These risks stem from cyclical and political events that are expected to combine and influence the UK’s economic and construction prospects. Upside risks to tender prices still exist, though, from a combination of supply-side (resource constraints) and demand-side issues (sector dynamics).

The price forecasts are based on key assumptions: the present construction output trend continues its drift downwards but not falling precipitously; principal contractor order books are filled but through greater flexibility in the accepted commercial terms rather than significant price changes; uncertainty (both cyclical and Brexit-related) begins to introduce genuine turbulence into the UK economy; prevailing trends in government capital expenditure are not substantially increased over the short term and into the medium term; and sterling sees on-going fluctuations while continuing to strengthen against the US dollar but not against the euro.

B / ICAEW UK Business Confidence Index

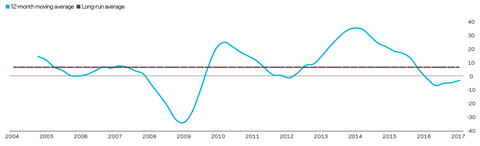

C / Tender price inflation (yearly run rate and forecasts)

Percentage change at Q4 on a year earlier (12-month periods). Baseline forecast 50%/70%/90% probability distributions shown

No comments yet