- Home

- News

All the latest updates on building safety reformRegulations latest

- Focus

Close menu

- Home

- News

- Focus

- Comment

- Events

- CPD

- Building the Future

- Jobs

- Data

- Subscribe

- Building Boardroom

Market forecast Q4 2018: Losing confidence

By Michael Hubbard2019-02-14T06:00:00

Tender prices in the year to Q4 kept climbing in the wake of rising building costs, as construction output rebounded in Q3 – but new orders dropped

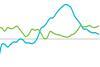

01 / Summary

Tender price index ▲

Tender prices increased by 3.5% over the year at Q4 2018. Construction price inflation is still clearly present in the supply chain and remains a source of commercial tension.

Building cost index ▲

A composite measure of building input costs recorded a 4.7% yearly rate of change in Q4 2018. Demand for construction labour and materials, combined with weaker sterling and its effect on imports, are creating commercial pressures for the supply chain.

Consumer prices index ▲

The annual rate of change eased to 2.1% in December 2018. The yearly rate of change is continuing to move towards its target, which helps real wage growth in construction and the economy more broadly.

…

This is PREMIUM content

available to Building Boardroom and Building subscribers only

You are not currently logged in. Building Boardroom Members and Subscribers may LOGIN here.

Become a Building Boardroom Member

to read this report now, plus have unlimited access to:

- Exclusive research and client insight to support your strategic planning

- Benchmark reports, and proven tools to aid your business development

- Attend bespoke community events…plus much more

Alternatively…

Become a Building subscriber

to gain access to building.co.uk for the latest news, expert analysis & comment from industry leaders, plus data and research.

Already a Boardroom member? Log in here.