Outgoing Qinetiq chief executive Leo Quinn promises to ‘restore Balfour Beatty to its rightful place on the global stage’

The City has hailed Balfour Beatty’s appointment of its new chief executive Leo Quinn as he promised to “restore Balfour Beatty to its rightful place on the global stage”.

On Wednesday the firm announced Quinn, who is currently chief executive of listed defence technology contractor Qinetiq, will join Balfour Beatty from 1 January next year.

The appointment is seen as key for Balfour Beatty, after having gone through a turbulent few years which have seen it issue five profit warnings, the departure of two chief executives and the impending departure of executive chairman Steve Marshall.

Quinn, who began his career at Balfour Beatty as a civil engineer in 1979, has been credited with playing a key role in turning around Qinetiq over the five years he has been in charge. Prior to working at Qinetiq, Quinn was chief executive of banknote publisher De La Rue from 2004-2008, and has spent time in senior roles at technology firms Honeywell and Invensys.

Stephen Rawlinson, analyst at Whitman Howard, said: “The appointment both on paper given Leo Quinn’s background and on what we have seen and heard from him over the years is as good as Balfour Beatty could have got, in our view.”

Quinn’s appointment initially caused Balfour Beatty’s share price to jump 13% but this then fell back to a 5% gain as Building went to press on Wednesday, close to recent lows.

In a letter to the firm’s 40,000 staff, seen by Building, Quinn summarised what his approach would be when managing the firm.

He acknowledged that the firm had suffered “major setbacks recently” but said he would “invest for growth beyond the near and now” and “focus on our strengths, our customers and the longer-term”.

He said: “My commitment to you is this: I will restore Balfour Beatty to its rightful place on the global stage and do this company of people proud.”

Steve Marshall said Quinn had the “depth and breadth of experience” to turn the company around. “Leo is an outstanding individual with an excellent track record in improving the performance of major international businesses. I am confident that Balfour Beatty will thrive under Leo’s leadership,” he said.

The news came just days after the firm warned shareholders that if they fail to back the sale of its consultant arm Parsons Brinckerhoff the contractor could edge close to breaching its banking covenants.

In a circular to shareholders, issued last week, Balfour Beatty set out its strategy for the sale of Parsons for £820m to Canadian-based consultant WSP.

The sale of the consultant will mean Balfour can return “up to £200m” of the proceeds to shareholders, with £85m used to cut the group’s pension funds deficit and £80m swallowed up by transaction costs.

The remainder will be retained by Balfour to “ensure a strong balance sheet and provide increased financial flexibility”.

Balfour Beatty said: “If shareholders do not approve the transaction, the group is expected to have less headroom on net debt to Ebitda covenants given as part of its funding arrangements.

“In this scenario, should there be a further modest deterioration in the profitability of the group, and in the absence of any mitigating action, there may be a breach of the net debt to Ebitba covenants.”

Balfour Beatty said there was “a number of mitigating actions which can be taken to address the potential risk of such a covenant breach”, including accelerating the sale of investments.

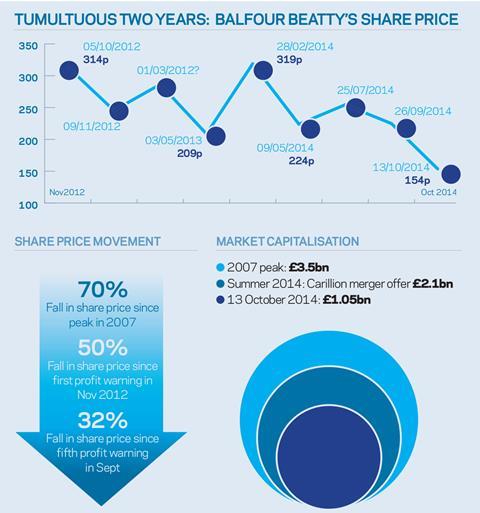

The £10bn-turnover construction giant’s market capitalisation had, by early this week, sunk to £1.07bn – down from the £1.3bn it fell to following the £75m profit warning last month and around half the price at which Carillion valued the business in its merger offer in the summer, which Balfour Beatty rejected in August (see chart, above).

The market capitalisation, as Building went to press, is below the level of the firm’s PPP asset portfolio - before the disposal of its 50% stake in a West Yorkshire PFI hospital – which the firm revised up by 46% to £1.1bn in August.

Balfour Beatty appoints Quinn: What the analysts think

Stephen Rawlinson, analyst at Whitman Howard

The turnaround at Qinetiq over the five years that Quinn has been in charge has parallels with what Balfour Beatty is trying to achieve. “A stronger more focused group” is what Balfour Beatty says it is trying to achieve, but in fact those are the words on the front of Qinetiq’s last annual report.

The first tasks will be to get to the bottom of likely contract performance and liabilities not just in the UK but also in all other businesses and make some senior appointments of his own team.

Joe Brent, analyst at Liberum

This is potentially one of the great corporate turnarounds of UK corporate history and while there is a risk/probability of more bad news on earnings, there is deep value and huge recovery potential.

Leo Quinn is widely recognised as a top-draw chief executive, who is particularly strong at working capital management, which is key for Balfour. The fact that he is willing to join Balfour at this time means that he can see value in the business, where many investors appear to have given up on it.

Andy Brown, analyst at N+1 Singer

Simplistically if you look at where he has been, from what I know about Qinetiq, it has large contracts and big customers and it had some problems when he went in and he has turned it around.

It’s good that Balfour Beatty has managed to find someone with that calibre for them because the challenge was that if you looked around the UK market there was no one obvious that they would go for.

Obviously new guys come in and they have their own way of doing things… I’m sure there’s a lot of people who are looking over their shoulder.

Kevin Cammack, analyst at Cenkos

Balfour Beatty takes some pride by referring to Leo as a Balfour Beatty old-boy having started his career as a civil engineer in the UK construction division back in 1979.

I don’t know the man but credentials suggest that he’s a decent signing capable of making change.

The shares, now fully backed market cap-wise by PFI equity value, have a base for a short-term rally, although trading-wise things could get worse before they get better. However, as they say: “Where there’s life, there’s hope.”

No comments yet