Connectivity between the cities of China’s Pearl River Delta is key to economic development. Ciara Walker, Jim Sheerin, Weibin Xu, Francis Au and Diane Legge-Kemp from Arcadis discuss how investment in advanced infrastructure is creating the world’s first ‘megalopolis’

01 / Introduction

Covering less than 1% of land area, and housing less than 4% of the population of China, the nine cities of the Pearl River Delta (PRD), Guangzhou, Shenzhen, Foshan, Dongguan, Zhongshan, Zhuhai, Jiangmen, Huizhou and Zhaoqing, account for almost 10% of China’s GDP, almost 20% of its foreign direct investment and 25% of trade.

Previously known as the factory of Asia, the region is arguably the first large scale pilot of a hyper-connected, polycentric city region, a model believed by many to be the future of urban development.

Guangzhou and Shenzhen experienced huge growth in GDP (more than 750%) since opening to Western markets in the 1980s. The recent designation of Free Trade Zones alongside the £212bn investment in 150 major infrastructure projects in the region is providing the same opportunity to the remaining seven cities as they are connected to wider markets and investments, foreign and domestic.

| City-region Indicator | Data |

|---|---|

| Arcadis Sustainable Cities Index | 8th (Hong Kong |

| Profit | |

| GDP (£) | 690bn |

| Year-on-year economic growth (%) | 7.8% |

| Unemployment rate (%) | 3.4% |

| Class A office vacancy rate (%) | 18.9% |

| People | |

| Population (2015) | 60m |

| Population growth rate (annual %) | 0.4-1% |

| Total number of tourists | 294m (domestic) 33.6m (overseas) |

| Year-on-year tourist growth | 9.9% (domestic) -1.2% (overseas) |

| Planet | |

| Green electricity consumed as a % of total energy consumption | 10.3% |

| Greenhouse gas emissions (metric tons of CO2 equivalent) | 610.5 |

02 / Economic and political overview

The PRD is one of three “National Optimised Development Zones” in mainland China. However, the inclusion of Hong Kong (HK) and Macao in the Greater Pearl River Delta (GPRD) makes it the most globally integrated of the three. Huge growth in manufacturing since the 1980s made the PRD an export powerhouse, with higher export volume than France and an economy the size of Indonesia’s at more than £690bn. The manufacturing-led growth contributed to a high GDP per capita of £10,661 in 2014, more than double the national average, and economic growth of 7.9% – 1% faster than for China in 2015. Though the national slowdown in economic growth reduced demand for the region’s traditional outputs, the ongoing transition to high-tech and high-skilled manufacturing allowed above national average growth of 7.9% in 2015, and annual growth to 2020 is targeted at 7%.

Guangzhou and Shenzhen, the region’s two tier one cities, account for 41% of the urban population of the PRD and 57% of GDP. Four of the five cities on the West Bank of the delta are lagging behind without the strong connections to the markets of HK and Shenzhen on the East Bank.

As the nine cities at different stages of economic development grow into a megalopolis through investment in connectivity, a combination of regeneration and urbanisation is needed to bring all areas of the PRD up to the standards of its leading cities.

The importance of connectivity is clear: both Zhuhai and Shenzhen were among the first to be designated Special Economic Zones in 1980, and by 2013 Shenzhen, with its proximity to HK, had skyrocketed to £237bn GDP, compared to only £27.3bn in Zhuhai. With improved transportation, investment in industry, housing and office space will become more attractive outside of the main cities, driving growth in second tier cities. In particular, the West Bank of the PRD, with historically poor transportation, will benefit from improved connectivity, and can expect to see a boom in industrial and commercial investment.

The national and local government’s effective planning for specialisation in industry focus across the cities (led through the special economic zones) and planned infrastructure investment are spurring healthy competition for residents and businesses between the cities and smoothing urban development across the region. Local government aims to capitalise on its investment in infrastructure through better economic outcomes for its citizens, expecting GDP per capita to more than double to £24,828 by 2030.

The “new normal” is the Chinese national government’s strategy to shift China away from unsustainable high growth based on investment and low value added manufacturing and on to sustainable, slower growth based on domestic consumer demand and more innovative, higher value added manufacturing.

Strategic directions include:

- Slower, more sustainable growth

- Moving up the value chain

- Rise of the consumer class

- Digital revolution

- Urbanisation continues

- City competition

- Growth of domestic private enterprises

- Deregulation and reforms

- Anti-corruption measures

- A sustainable future.

The PRD has already embarked upon this transformation, leading the nation in becoming a centre for innovation with Shenzhen approaching a level of research and development (R&D) at 4% of GDP, not far off the world leaders in innovation (South Korea at 4.4%, Israel at 4.2%).

Three complimentary plans are guiding the development of the GPRD:

- At the national level the 13th Five Year Plan 2016-2020

- Guangdong provincial Five Year Plan 2016-2020

- City level plans

03 / Construction and Real Estate Market

The opening up through special economic zones and the increased connectivity to previously untapped areas are causing developers to look hard at the PRD as an area of opportunity. The construction market has experienced some deceleration due to the economic slowdown in China from 18% output value growth in 2014 to 9% in 2015, but remains strong. Developer interest is particularly evident on the West Bank where land prices are significantly lower, driving some land speculation ahead of an anticipated boom in construction once the Macau-Zhuhai-HK Bridge is complete (expected in late 2018).

Construction output value in Guangdong province (in which the PRD is situated) has grown on average by 16.6% per year since 2011 and there are questions as to the capacity in the region to continue to respond to such strong growth. In particular, the labour market is a challenge, with the average age continuing to grow and a lack of desire to enter into what is considered an unattractive profession.

With the existing infrastructure construction pipeline and the expectation of a surge in real estate construction across the cities as they become better connected, labour shortages will only get more acute and are already contributing to delays in prestige projects such as the HK-Guangzhou express railway.

The market remains dominated by Chinese companies who can, in many cases, build cheaper and faster than foreign companies. Due to restrictive licencing conditions it remains a difficult and lengthy process for foreign construction companies to receive a full licence to operate.

As the “new normal” progresses, and quality continues to grow in importance compared to speed, foreign companies are increasingly engaged to lend expertise, mostly in a consultative role.

Though improving, there are still safety and regulatory issues, for example the Shenzhen landslide caused by construction waste piled up on a hill. These are being addressed through anti-bribery legislation and improved building regulations.

04 / Infrastructure

Transportation will be the economic backbone of the region and regeneration is planned around the transportation corridors to avoid isolated communities and maximise the benefits of investment. The National Development and Reform Commission (NDRC) has ambitious plans for a “one hour commuting circle” twice the size of Wales, ensuring connection between all the cities within one hour through high speed rail connections and the expansion of expressways. Chinese expertise in large scale infrastructure construction is helping meet the target. With Guangzhou at its core, 23 high speed railways will integrate the cities into a diverse polycentric region with multiple industries for investment and multiple locations for citizens to work, play, live, and learn, all within one hour of travel. Of these, 16 (or 1,480km) are to be completed by 2020. The HK-Zhuhai-Macao Bridge will open up the comparatively underdeveloped West Bank of the Pearl River Delta. An additional bridge between Shenzhen and Zhongshan will start in 2016 and be finished by 2021, connecting the West Bank further. Further connectivity will be ensured with investment in intra-city travel by Guangzhou, Shenzhen and Dongguan. Guangzhou will have the largest (20 line) metro network in the GPRD by 2040. Thirteen routes with a combined length of 228.9km have been approved by the NDRC at a cost of £129bn. The local government in Shenzhen is building a 720km, 20 line metropolitan system with 10 lines to be completed by 2016.

Table 1: Major Infrastructure Projects in the PRD

| Connectivity | Infrastructure | Selected major projects under construction/planning |

|---|---|---|

| Within the PRD and Guangdong province | Railways | High-speed railways to Nanning, Guiyang, Xiamen and Maoming |

| 1,890km of intercity railways linking the cities and major towns in PRD | ||

| Metros or urban transits in Guangzhou, Shenzhen and Dongguan | ||

| Expressways | 1,110 km of national network and 3,410km of provincial network to be completed by 2016 | |

| Cross-boundary links in the GPRD | Railways | Guangzhou-Shenzhen-HK Express Rail Link |

| HK – Shenzhen Western Express Line | ||

| Expressways | HK – Zhuhai – Macao Bridge | |

| Liantang/Heung Yuen Wai Boundary Control Point | ||

| International and external connectivity | Airport development | The 3rd, 4th and 5th runways of Guangzhou Baiyun airport and its neighbouring economic zone |

| Third runway of Hong Kong International airport | ||

| Third runway of Shenzhen Bao’an International airport | ||

| Container terminals | Phase 3 of Nansha Port in Guangzhou | |

| Container ferry in Yantian Port and phase 2 of Dachanwan Port in Shenzhen |

05 / Social Infrastructure

The household registration system (hukou) in China allows social services, including education, health, and so on, to be accessed only in an individual’s city of origin and birth. Guangdong province government has progressive plans to integrate household registration across the PRD. They are allowing the population to obtain social services anywhere within the city region, further interlinking communities and allowing access to healthcare and education for migrants who previously could only access these illegally in the PRD.

Demand for social services will increase once economic migrants can access them legally anywhere within the region, presenting a significant challenge for local governments with respect to affordability and expansion of capacity of social services.

The innovation focus in the “new normal” strategic direction requires significant investment in the education system to support the innovative and high tech industries flocking to the PRD.

As part of this investment, the next phase of development in Longguan (Shenzhen) will be an urban park and planned university centre for as many as 10 international universities, of which two are already being built.

06 / Industrial

An essential part of the “new normal” is the move towards higher value added manufacturing. The heavily industrial PRD is at the centre of this and local government is already pivoting away from low-skilled manufacturing due to the global slowdown and subsequent reduction in demand for its traditional exports. Industry’s contribution to GDP has grown from 36% in 1980 to 43% in 2014, and the tertiary sector from 25.7% to 49%, a clear shift in composition. As such, retooling of declining industrial and logistics parks is necessary to make the best use of existing land as low-skilled manufacturing moves further inland and higher specification facilities are demanded. In some areas this is already under way, for example the development zones in Foshan have been integrated into one national-level high tech zone and six provincial level development zones. The wave of industrial upgrading in the PRD means well facilitated large-scale industrial parks with professional services have begun to predominate across the region. The PRD has also seen significant growth in logistics stock during this transition, with 41.78% growth in stock over the three years to 2014, to 6.38 million m2.

Improved connectivity across the region will allow the cities to develop their own specialised industries while benefiting from the cluster effect of the world class supply chain which already exists in the PRD, feeding off each other’s success whilst competing for business.

Shenzhen and Guangzhou dominate the logistics hierarchy with 3 million and 1.9 million m2 respectively, whilst Dongguan, Foshan and Huizhou are building capacity to support their roles as massive manufacturing hubs.

Table 2: Industrial Property rent in PRD

| Shenzhen | Guangzhou | Foshan | Zhuhai | Dongguan | Huizhou | |

|---|---|---|---|---|---|---|

| Facilities rental (£ per m2 per month) | Average 3.72 | Average 2.83 | Warehouse 1.28 – 2.13 | W 1.17 - 1.91 | W 1.17 - 1.91 | W 1.17 – 2.13 |

| Factory 1.38 – 1.59 | F 1.38 – 1.59 | F 1.38 – 1.59 | F 0.96 - 1.38 |

07 / Commercial

The huge growth of the tertiary sector to 49% of GDP has driven strong demand for office space particularly in Shenzhen and Guangzhou.

Shenzhen and HK will be the world’s largest banking city cluster by 2025, ensuring continued demand for office space in the region. Shenzhen has seen an explosion in commercial space in Qianhai, its financial and professional services development zone. Demand in Shenzhen continued to grow with net absorption rate increasing by 180% from 2014-2015. A further 1.56 million m2 is expected to be added in 2016 in Guangzhou and Shenzhen alone as demand for office space remains strong.

In lower tier cities in the region, few wholly commercialised office buildings built by developers appeared until recent years, when a rush to build commercial space left many new CBDs with high vacancy rates.

The investment in connectivity in the region, as well as the “new normal” shift towards higher value-added industry and the tertiary sector will provide significant momentum for the prime office market, and demand is expected to be strong despite the economic slowdown in China.

Table 3: Commercial property market in PRD

| Shenzhen | Guangzhou | Zhuhai | Foshan | Huizhou | Dongguan | |

|---|---|---|---|---|---|---|

| Stock (m2) | 2,500,000 | 2,750,000 | 250,000 | 370,40 | 391,000 | 842,000 |

| Monthly rents (£ per m2) | 22.85 | 16.51 | 5.31 – 7.97 | 4.25 – 7.44 | 4.25 – 7.44 | 3.72 - 7.44 |

| Major development | Ping An Finance Centre | Chow Tai Fook Centre | Yanlord Marina Centre | Jinhai Plaza | China Central Place | Hyphen Commercial Centre |

08 / Retail

The PRD is a centre for retail in mainland China, with 7.9% of national retail sales and the highest number of online shoppers, as well as significant (10.9%) growth in retail sales in 2014. The region saw a boom in shopping centre construction over the past 10 years as disposable income and the middle class grew. By the end of 2005, for example, Dongguan had over 12 large shopping centres clustered in 4 downtown retail hubs. The rapid development of retail real estate resulted in many sites with unsatisfactory performance, therefore alongside the current boom in retail space development in Shenzhen and Guangzhou developers are also adapting and updating poorly suited malls built during the initial rush of demand. At least 1.16 million m2 of additional retail space is planned for 2016 in Shenzhen and Guangzhou alone. The retail real estate market has shifted in the region from a focus on quantity of supply to quality, with emphasis on lifestyle and entertainment centres as opposed to simply retail stock.

Table 4: Retail property market in PRD

| Guangzhou | Shenzhen | Zhuhai | Foshan | Dongguan | Huizhou | |

|---|---|---|---|---|---|---|

| Ground floor rental (£ per m2 per month) | 113 | 97 | 31.9 – 47.8 | 21.3 – 29.8 | 21.3 – 31.9 | 15.9 – 26.6 |

| Stock (large scale retail properties with retail GFA > 30,000m2) | 2,000,000 | 2,250,000 | 233,000 | 1,428,000 | 1,600,000 | 419,000 |

| Major development | Parc Central | Sinus Iridum Palace | Bossanova Shopping Centre | Nanhai Vivo City | Pasadena Lifestyle Centre | Kaisa Centre |

09 / Residential

The residential market is mixed across the PRD region. Shenzhen and Guangzhou have active markets whilst second tier cities’ markets lag behind. Second tier cities have recently emerged as key expansion regions for well-known developers from Shenzhen and Guangzhou such as Vanke, China Overseas and R&F Properties. Overseas developers and investors are also extending footprints into these property markets, including CapitaLand and ING Group. However, due to the current economic situation and the success of domestic players, this expansion has decelerated. The investment in transport infrastructure over the next Five Year Plan will make a big impact on these markets, with improved connectivity allowing for more efficient distribution of the population across cities and driving an uptick in previously underdeveloped residential markets.

Though China’s residential development regulations remain strict, incentives to residential development, including successive interest rate reductions, have been put in place by the local and national government. These measures are feeding into increased supply and demand in the prime residential markets of Shenzhen and Guangzhou. Significant development of prime residential real estate will be needed to meet demand from the highly educated talent the “new normal” economic policies are attracting.

Table 5: High-end residential markets in the PRD

| Shenzhen | Guangzhou | Zhuhai | Dongguan | Foshan | Huizhou | |

|---|---|---|---|---|---|---|

| Price range (£ per m2) | Average 3,552 | Average 1,841 | Apartment 1,382 -2,657 | Apartment 1,063 -1,913 | Apartment 1,010 -1,700 | Apartment 744 - 1,594 |

| Villa 1,594 – 3,719 | Villa 1,594 -4,251 | Villa 1,275 – 4,251 | Villa 1,063 - 2,657 | |||

| Major development | One Shenzhen Bay | Forest Hills | Vanke Hills | Top of the World Phase III | CITIC Lake | Hopson Regal Riviera Bay |

10 / Conclusion

The sheer scale of the challenge of developing an urban area of 41,000km2, 26 times larger than Greater London, is difficult to comprehend.

When you factor in the 80 million people expected to live in the GPRD by 2020, the importance of planned investments in infrastructure, social infrastructure, commercial and industrial space and housing becomes clear.

Improved connectivity throughout the region allowing its citizens wider options for employment, housing, leisure and social services is ensuring no one city becomes overburdened. Investment in expansion of central business districts and industrial parks across the region will also help to rebalance uneven development across the PRD.

As China transitions to the “new normal”, the PRD is making the investments necessary not only to satisfy the needs of a more sustainable growth model, but also to serve as a model for polycentric city region development. The PRD is at the heart of China’s transformation and is dependent upon its successful transition to a more sustainable model.

As a pilot for the future of urbanisation, we can expect to see more growth and innovation from the Pearl River Delta. City regions worldwide, such as the UK’s northern powerhouse, should look to the PRD as a model for planning investment on a megalopolis scale.

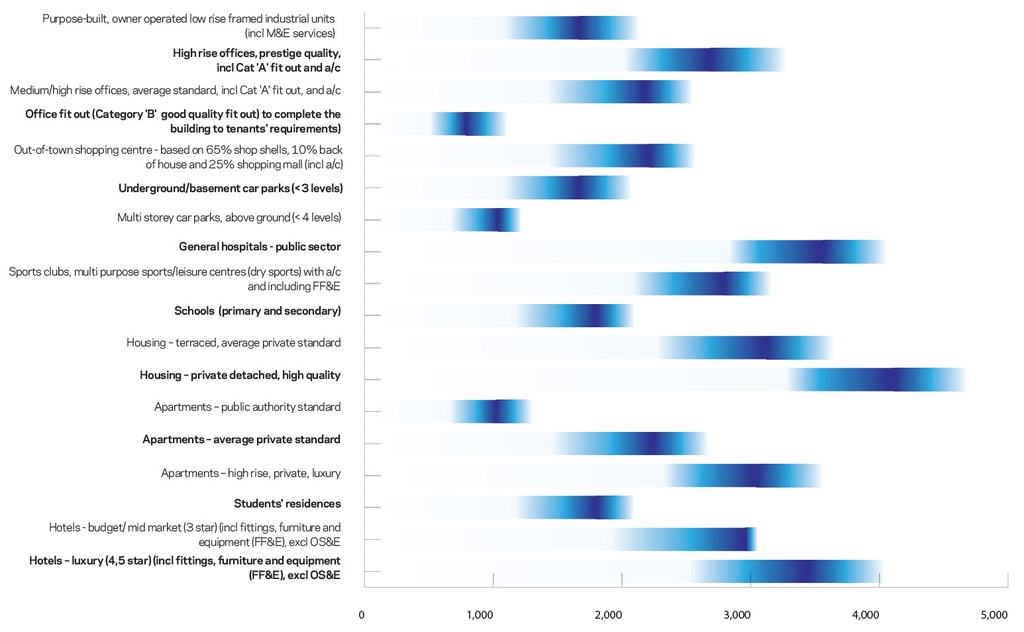

Table 6: Indicative costs per m2 in Pearl River Delta (costs in £ per m2)

No comments yet