Residential and civil engineering worst hit by global uncertainty

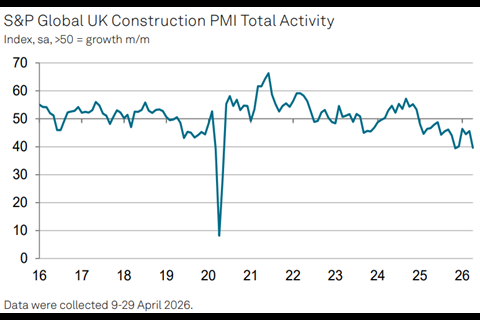

Business activity decreased in April and cost inflation hit its highest level since June 2022, according to the latest construction PMI data.

S&P Global’s purchasing managers’ index, which tracks changes in activity, registered 39.7 in the month, down from 45.6 in March.

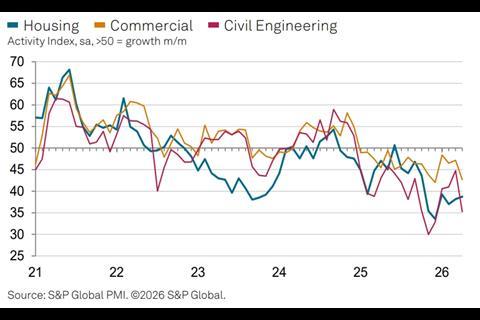

The latest output reading was the weakest for five months, with civil engineering and housebuilding registering the steepest declines and commercial work comparatively resilient.

Survey respondents reported subdued demand conditions and elevated uncertainty due to the Middle East conflict, with total new business seeing its sharpest decline since November 2025.

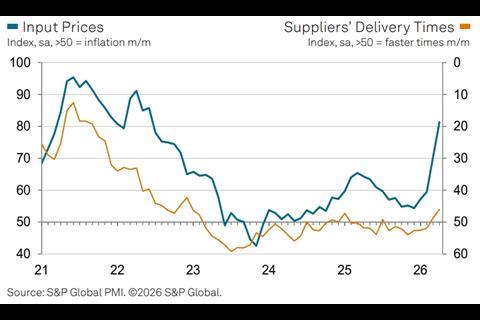

Supply chain challenges were also noted, with the sharpest increase in average lead times since December 2022 attributed to shipping delays and the difficulty of imported materials from the Gulf region.

Fuel surcharges also contributed to increases in purchasing costs, with 69% reporting a rise in input costs in April, up from 48% in March.

Tim Moore, economics director at S&P Global Market Intelligence, said: “Aside from the post-pandemic surge in input prices from early-2021 to mid-2022, the latest rise in purchasing costs was the steepest in three decades of data collection.

“April data again signalled subdued underlying demand conditions, despite construction companies reporting pockets of growth in areas such as energy infrastructure work. A lack of new orders to replace completed projects contributed to the sharpest decline in business activity for five months.”

Business activity expectations also softened to their least optimistic point since November 2025, though some firms expressed hopes of a rebound in demand if the Middle East conflict subsides.

Atul Kariya, head of real estate and construction at MHA, said housebuilders were being particularly impacted “as higher input costs hit supply chains just as buyer confidence and mortgage affordability come under strain”.

“The bigger issue across the sector is not just margins, but uncertainty which is delaying project starts and investment decisions,” he said, predicting that activity was likely to remain subdued until inflation and financing conditions improve.

Brian Smith, head of cost management at AECOM, said the dip in output was “troubling” given that spring is typically a period “when activity typically starts to pick up”.

He said the hold in interest rates would “keep pressure on developers and buyers” but make for a more predictable backdrop for investment decisions”, while noting that today’s elections in the UK could “threaten further decline” if they result in planning delays.

Huda As’ad, Accenture’s capital projects and infrastructure lead in the UK, said the steep decline was a “sharp reminder that the sector is still struggling to build sustained momentum” and said that firms needed to act now to increase productivity by “embracing digital”.

Meanwhile, data analyst Glenigan’s latest construction index showed the value of work starting on site in the three months to April had dropped 9% on the preceding three months.

Residential construction starts fell 8% on the preceding three months and were 33% down on 2025 figures.

Glenigan’s economics director, Allan Wilen said investors were “reassessing their development” due to global uncertainty, with residential and civil engineering particularly impacted.

“However, whatever the outcome of the coming weeks, there’s a general consensus that there will be fewer opportunities in the back half of this year, which also implies far fiercer competition,” he said, urging firms to “start seriously considering their own game plans and how they can stay afloat during an upcoming period of disruption”.

No comments yet