Costing Steelwork is a series from BCSA, Steel for Life and Aecom that provides guidance on costing structural steelwork. This quarter provides a construction market update by Dr Michael Sansom based on recent CPA forecasts, and data on prices and costs from Pablo Cristi Worm of Aecom

Click here to read the full costing report

The UK construction market is set to experience modest recovery and gradual growth through to 2027, following a difficult period of high inflation, elevated interest rates, labour shortages and weak commercial confidence. Growth is likely to be uneven, with infrastructure, industrial and data centre construction performing strongly, and traditional commercial and residential markets more subdued.

Total UK construction output is now forecast to fall by 2.5% in 2026; a sharp decline from the 1.7% growth forecast at the start of the year. After a weather-affected Q1, this fall is mainly due to the conflict in the Middle East. Although there is a time lag, Q2 is highly likely to see a drop in demand and sharp cost rises. How long the global disruption and high oil and energy prices last is uncertain, making accurate forecasting tricky. However, the uncertainty is already impacting construction projects and pipelines.

In addition to the Middle East conflict, underlying risks and constraints persist, including:

- Contractor insolvencies: while slightly down, there were 3,851 construction insolvencies in the year to February. Of more concern is the uptick in insolvencies in February; up 8.7% from January.

- Building Safety Regulator delays: progress has been made in the gateway 2 approval rate, but three- to four-month delays are reported for gateway 3.

- Skills and labour shortages: the UK construction workforce remains largely flat. The key issue in the medium term, as construction hopefully recovers, is the growing need for skilled workers. Although government has announced £625m to train 60,000 more skilled workers, there is a lack of teachers for new entrants, and construction apprenticeship drop‑out rates remain high: 50% for men and over 70% for women.

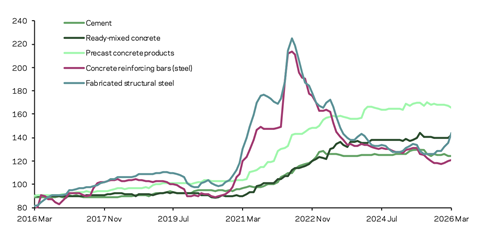

Material price inflation has risen sharply in 2026 and is likely to continue. The energy price spike in 2022, after Russia invaded Ukraine, led to a CPI of 11.1% and construction material inflation of 25.3%. CPA’s current “most realistic” scenario suggests a 14%-16% price increase on top of the 2.1% rise in February.

Although impacts will be product-specific, some energy-intensive product manufacturers have already highlighted that energy cost rises are likely to lead to double-digit percentage increases in prices. Steel section prices have risen by around 30% so far in 2026, and this may increase further after new UK and EU steel import quotas and tariffs are applied on 1 July.

Figure 1: Material price trends

Price indices of construction materials 2015=100. Source Department for Business and Trade

Infrastructure, the third-largest construction sector, was worth £34.6bn in 2025. Energy generation and, especially, National Grid distribution work continue to grow at double-digit rates each year. Output is expected to increase steadily over the forecast period, driven by investment to enhance and expand the UK’s energy, water and sewerage infrastructure; rising by 3.2% in 2026 and 3.4% in 2027. Viability remains stretched in privately financed sub-sectors, including offshore wind, and publicly funded transport projects are likely to be especially sensitive to cost inflation.

After a strong 2025, industrial output is forecast to fall 2.4% in 2026, then rise 0.6% in 2027. The sector peaked in 2022 due to “smart warehouse” projects and manufacturers investing in new facilities after strong demand and global supply chain difficulties. While a pipeline of small and medium-sized warehouse and factory projects remains, most growth has been driven by other areas. Data centre investment is set to increase fourfold between 2024 and 2029. Large projects and hyperscale data centres have been announced in the last 12-18 months, but grid capacity and competition for land with other industrial uses may hinder growth.

The outlook for the commercial sector has weakened as the economic impacts of the conflict in the Middle East worsened uncertainty and business confidence fell. Prolonged investor caution and the prospect of higher build and finance costs are expected to delay the start of large new-build projects, such as office towers, leading to another downgrade in the commercial output forecast.

Commercial output is forecast to fall by 3.7% in 2026 with a modest 0.5% rise predicted for 2027.

Activity on smaller, high-end, high-value refurbishment and fit-out projects remains strong and is likely to grow further, as agents are widely anticipating a lack of grade A quality office space in 2028 and Minimum Energy Efficiency Standard requirements mean that by 2030, around 70% of the existing office space may end up as “stranded assets”.

Figure 2: Tender price inflation, Aecom Tender Price Index, 2019=100

| Forecast | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Quarter | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | 2026 | 2027 | 2028 |

| 1 | 99.2 | 101.4 | 101.0 | 110.4 | 122.4 | 122.7 | 126.3 | 130.7 | 135.8 | 139.8 |

| 2 | 99.5 | 101.8 | 103.2 | 113.2 | 123.4 | 123.7 | 127.5 | 131.7 | 136.8 | 141.1 |

| 3 | 100.4 | 100.2 | 105.5 | 116.2 | 123.5 | 124.7 | 128.5 | 133.0 | 137.7 | 142.4 |

| 4 | 100.9 | 100.2 | 107.3 | 119.8 | 122.5 | 125.7 | 129.4 | 134.5 | 138.5 | 143.8 |

Impacts on structural steelwork sector

For the structural steelwork sector, the outlook is challenging, with rising input costs, geopolitical instability, and shifting regulatory requirements.

- Material cost volatility – steel prices remain exposed to energy costs, global overcapacity, trade measures and carbon-related policies such as EU and UK CBAM.

- Import competition and trade policy – new UK steel safeguard quotas and EU trade measures may affect supply dynamics and pricing for sections, plate and fabricated steelwork.

- Embodied carbon pressures – clients increasingly want lower-carbon steel and robust environmental data such as EPDs, with greater supply chain transparency.

- Supply chain resilience – uncertainty on UK steel production capacity, alongside growing dependence on imports, could increase procurement risks.

- Labour and skills shortages – recruitment challenges continue across fabrication, welding and erection.

While the combination of thin margins and rising costs has put construction companies and the supply chain at risk of financial distress, on the positive side, several of the fastest-growing construction sectors are inherently steel-intensive.

Sourcing cost information

Cost information is generally derived from a variety of sources, including similar projects, market testing and benchmarking. Due to the mix of source information it is important to establish relevance, which is paramount when comparing buildings in size, form and complexity.

Figure 3 represents the costs associated with the structural framing of a building, with a BCIS location factor of 100 expressed as a cost/m² on GIFA. The range of costs represents variances in the key cost drivers. If a building’s frame cost sits outside these ranges, this should act as a prompt to interrogate the design and determine the contributing factors.

The location of a project is a key factor in price determination, and indices are available to enable the adjustment of cost data across different regions. The variances in these indices, such as the BCIS location factors (figure 3), highlight the existence of different market conditions in different regions.

To use the tables:

1. Identify which frame type most closely relates to the project under consideration

2. Select and add the floor type under consideration

3. Add fire protection as required.

For example, for a typical low-rise frame with a composite metal deck floor and 60 minutes’ fire resistance, the overall frame rate (based on the average of each range) would be:

£193.00 + £139.00 + £35.50 = £367.50

The rates should then be adjusted (if necessary) using the BCIS location factors appropriate to the location of the project.

Figure 3: Indicative cost ranges based on gross internal floor area

| TYPE | Base index 100 (£/m2) | Notes |

|

Frames |

||

|

Steel frame to low-rise building |

178-208 |

Steelwork design based on 55kg/m2 |

|

Steel frame to high-rise building |

290-340 |

Steelwork design based on 90kg/m2 |

|

Complex steel frame |

355-415 |

Steelwork design based on 110kg/m2 |

|

Floors |

||

|

Composite floors, metal decking and lightweight concrete topping |

118-160 |

Two-way spanning deck, typical 3m span with concrete topping up to 150mm |

|

Precast concrete composite floor with concrete topping |

146-206 |

Hollowcore precast concrete planks with structural concrete topping spanning between primary steel beams |

|

Fire protection |

||

|

Fire protection to steel columns and beams (60 minutes resistance) |

30-41 |

Factory applied intumescent coating |

|

Fire protection to steel columns and beams (90 minutes resistance) |

47-76 |

Factory applied intumescent coating |

|

Portal frames |

||

|

Large-span single-storey building with low eaves (6-8m) |

115-150 |

Steelwork design based on 35kg/m2 |

|

Large-span single-storey building with high eaves (10-13m) |

140-180 |

Steelwork design based on 45kg/m2 |

Figure 4: BCIS location factors, as at Q2 2026

| Location | BCIS Index | Location | BCIS Index |

|

Central London |

122 |

Nottingham |

103 |

|

Manchester |

105 |

Glasgow |

93 |

|

Birmingham |

97 |

Newcastle |

89 |

|

Liverpool |

100 |

Cardiff |

102 |

|

Leeds |

94 |

Dublin |

90* |

*Aecom index

Steel For Life sponsors

CBAM and construction

Why the construction industry needs to pay attention to carbon border taxes

The construction industry is becoming increasingly familiar with carbon measurement, embodied emissions and net zero targets. Yet one of the most significant policy changes affecting material supply chains has received relatively little attention outside specialist circles: the Carbon Border Adjustment Mechanism, better known as CBAM.

For many in construction, CBAM may sound like another piece of environmental bureaucracy. In reality, it represents a fundamental shift in how carbon costs are incorporated into international trade and could have major implications for steel prices, procurement decisions and supply chains over the coming decade. While its direct impact on many contractors may initially be limited, the indirect effects could be significant.

The EU has already introduced EU CBAM, and the UK plans to follow in 2027. For an industry that relies heavily on imported steel, aluminium and other energy-intensive materials, understanding the basics of CBAM is increasingly important.

What is CBAM and why is it being introduced?

At its core, CBAM is designed to address something called “carbon leakage”. This occurs when carbon-intensive manufacturing shifts from countries with strict climate regulations to countries with weaker environmental policies and lower carbon costs.

For example, if steel producers in Europe are required to pay a high carbon price under emissions trading schemes, imported steel from countries without similar carbon pricing can gain an unfair cost advantage. In effect, manufacturing emissions are simply relocated elsewhere rather than genuinely reduced.

CBAM attempts to level the playing field by imposing a carbon-related cost on imported products. The idea is simple: imported materials should face a carbon cost comparable to those produced domestically.

EU CBAM is the first major system of its kind and signals a major change in how international trade will work for carbon-intensive sectors including steel, cement, aluminium and fertilisers. While climate policy has historically focused on domestic emissions, CBAM extends carbon pricing into global supply chains.

The timeline: Europe first, the UK next

The EU began a transitional phase of EU CBAM in October 2023, initially requiring emissions reporting but not payment. From 1 January 2026, the system moved into its “definitive” phase, meaning EU importers now face financial obligations linked to embedded carbon in imported goods.

The UK is set to introduce its own UK CBAM on 1 January 2027, largely following a similar approach to the EU but with some important differences still being finalised. Importantly, UK CBAM has no transitional phase and the UK CBAM tax will accrue from 1 January 2027. The UK system will function as a tax administered by HMRC.

Other countries, including Canada, Australia, Japan and Turkey, are also exploring their own border carbon mechanisms, suggesting CBAM-type systems could eventually become a normal feature of global trade. In other words, this is not a short-term regulatory trend – it is part of a wider shift in how international manufacturing and imports are governed.

Why steel matters so much

For the construction sector, steel is likely to be the biggest material affected by CBAM. Steel production is energy-intensive, particularly when produced using the traditional blast furnace route. Because of this, iron and steel products are among the highest-priority materials within both the EU and UK CBAM frameworks.

Importantly, CBAM does not just apply to raw steel. It also applies to a wide range of downstream steel products used in construction.

This means construction supply chains may increasingly need to understand not just where steel comes from, but how it was manufactured and what carbon has been emitted during its production. Procurement teams that traditionally focused on price, lead time and quality may soon need to include carbon transparency as another key purchasing consideration.

The link between CBAM and carbon pricing

To understand CBAM, it helps to understand emissions trading schemes (ETS).

An ETS effectively places a price on carbon emissions. Companies in sectors such as steel manufacturing receive or buy allowances for emissions and can trade these permits in a carbon market.

Both the EU and UK operate emissions trading schemes, but they currently have different carbon prices. In early 2026, the EU ETS price stood at approximately €73 per tonne of carbon dioxide, while the UK ETS price was around £50 per tonne. This difference matters because the CBAM cost on trade between the UK and the EU is a function of this variation.

In simple terms, CBAM charges are designed to reflect the gap between carbon prices in different jurisdictions. If a UK steel producer exports to the EU and the UK carbon price is lower, an adjustment may be required at the border.

This has created growing pressure for greater alignment between the UK and EU carbon markets. Formal negotiations on linking the UK and EU ETS systems began in 2026. If successful, such alignment could potentially remove CBAM costs for UK-EU trade altogether, providing much-needed certainty for businesses operating across borders.

What does this mean for construction costs?

This is the question many businesses are asking. In the short term, direct impacts on most steelwork contractors may be relatively modest. However, indirect impacts are likely to become more noticeable.

Steel suppliers, stockholders and manufacturers are already dealing with new administrative requirements and carbon-related costs. These additional burdens are expected to feed through into material pricing.

For construction clients and contractors, this could translate into:

- Higher steel costs

- Greater price volatility

- Increased procurement complexity

- Pressure to source lower-carbon materials

- More scrutiny of imported products.

The result is another layer of uncertainty in an industry already dealing with inflation, geopolitical risks and supply chain disruption.

Why emissions data suddenly matters

Under the EU system, importers can either use verified “actual” emissions data from manufacturers or rely on default emissions values provided by regulators. Using verified actual data can significantly reduce costs if a producer has lower-than-average emissions. By contrast, relying on default values may be financially punitive.

This creates new expectations across supply chains. Construction businesses may increasingly find clients, suppliers or contractors asking detailed questions about the carbon profile and provenance of steel products.

In practical terms, the industry may begin to see carbon information becoming as important as mill certificates or CE/UKCA documentation. Knowing where steel came from – and how it was made – may become commercially valuable information.

The challenge of complexity

Although the principle behind CBAM is straightforward, the practical details are complicated.

Emissions can include direct emissions, indirect electricity-related emissions and emissions embedded within precursor products. Structural steelwork, for example, is treated as a “complex good”, meaning the embedded emissions of precursor materials – such as plate, sections and upstream steel production processes – also need to be considered. This level of complexity helps explain why many businesses are still trying to understand their obligations.

Even regulators are still refining some of the rules, particularly around emissions verification, reporting requirements and future scope expansions. From 2028, the EU plans to widen EU CBAM to include a broader range of downstream steel and aluminium products, potentially increasing the relevance for construction supply chains.

The UK construction perspective

For UK construction businesses, CBAM arrives at a time of major change in the steel market. The industry is already facing pressures from trade measures, steel safeguard quotas, rising energy costs, decarbonisation demands and uncertainty over domestic steelmaking capacity. CBAM becomes another piece in an increasingly complicated jigsaw.

There are also strategic questions around competitiveness. If the UK introduces CBAM later than the EU and with different pricing, this could temporarily alter trade flows. Some commentators believe global steel surplus may increasingly be diverted into the UK market in the short term, potentially lowering prices. Others argue UK producers could face growing competitive pressures if carbon-related export costs into Europe rise.

For construction clients seeking certainty over programme and cost, this creates another reason to engage early with supply chains and understand sourcing strategies.

What should the industry do now?

For most construction businesses, there is no immediate need to panic; CBAM is unlikely to radically transform project delivery overnight, particularly since CBAM costs will be phased in gradually as free allowances are phased out. However, ignoring CBAM would be a mistake since it is complex and can be an administrative burden.

Construction businesses should start by understanding which materials in their supply chain are within scope, particularly steel and aluminium products. Procurement teams should begin conversations with suppliers about carbon data availability, sourcing and likely future pricing impacts.

Contractors bidding for long-term projects may also want to consider how future carbon-related price movements could affect risk allowances.

Perhaps most importantly, the industry should recognise that CBAM is not simply a tax – it is part of a broader structural transition towards lower-carbon manufacturing and greater transparency in material supply chains.

The direction of travel is clear: carbon is becoming a cost that increasingly matters.

For an industry that consumes vast quantities of carbon-intensive materials, that shift will be impossible to ignore.

CBAM and construction: want to find out why the construction industry needs to pay attention to carbon border taxes?

The BCSA is hosting a webinar on this subject, presented by Dr Michael Sansom on 28 July 2026, from 1pm to 2pm.

The webinar will aim to provide an overview of the Carbon Border Adjustment Mechanism (CBAM) and its implications for the construction and structural steelwork sectors. It will explore how CBAM affects material costs, procurement strategies and supply chains, and what businesses should be doing now to prepare.

To register your attendance, click here.

Costing Steelwork is available at www.steelconstruction.info. The pricing data and rates contained in this article should be used for comparative purposes only and should not be used or relied upon for any other purpose without further discussion with Aecom. Aecom does not owe a duty of care to the reader or accept responsibility for any reliance on the contents of the article.

No comments yet