With costs rising over the year to Q4 2020 and tender prices falling, things have been tough for the construction sector. There are signs now of an increase in output, but ongoing uncertainty around covid lockdowns and Brexit red tape make the future harder to predict

01 / Summary

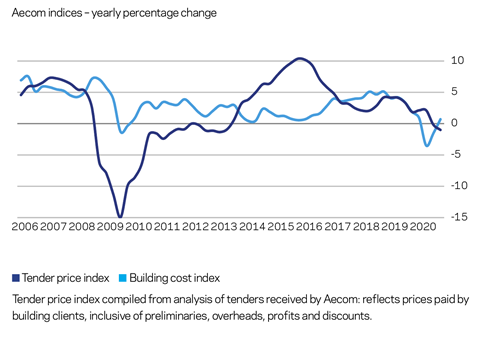

Tender price index ▼

Tender prices fell by just over 1% in the 12 months to Q4 2020. Pricing variability has increased, which is to be expected in a market seeing more competition.

Building cost index ▲

A composite measure of building input costs increased by 1.1% over the year at Q4 2020. Almost all materials classifications increased in cost, reflecting firm demand and inflationary pressures from Brexit.

Consumer prices index ▲

The 12-month rate of change was 0.6% in December 2020. Ongoing lockdown covid restrictions contributed to lower consumer activity and demand.

02 / Output

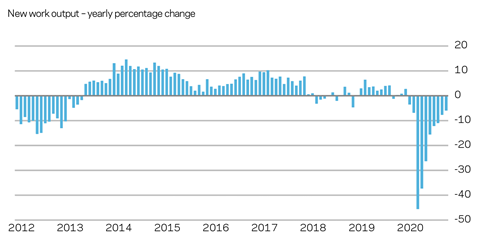

UK construction output

Construction output rallied relatively strongly throughout the second half of 2020, reflecting the return of aggregate construction activity as more sites either reopened or improved productivity against the backdrop of covid restrictions. The Office for National Statistics’ all-work construction output measure recorded a 41% increase between Q2 and Q3 2020, cancelling out the huge fall in output from the first lockdown.

The distracting feature to this improved output activity is that the data points remained negative on a yearly change basis. In other words, comparing the data point to the same time 12 months previously, aggregate output was smaller. The infrastructure subsector was by far the least affected in output falls across all of construction, making its path to achieving prior lockdown levels that bit easier.

Prior to the latest lockdown, some optimism existed for 2021 industry workload. However, this is not a uniform picture across all construction subsectors. This said, notable bullishness was evident in 2020 among some firms on their prospects for 2021. At the time, numerous contractors claimed to have already secured large parts of the order book comfortably within the 2020 calendar year. These views will depend in large part on a firm’s sector focus and related exposure to external events.

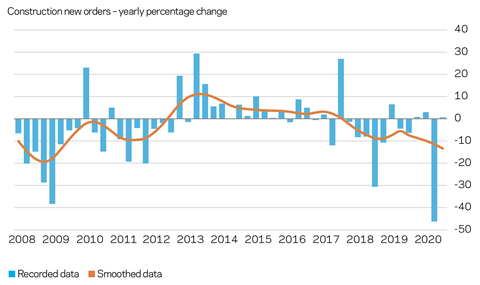

Orders, employment outlook and underlying demand paint a mixed picture, with some positive aspects and clear negative risks. New orders data in Q3 2020 improved marginally compared with the same point in 2019. This offers something of a bright spot, especially following the precipitous fall in recorded new orders in Q2 2020.

03 / Activity indicators

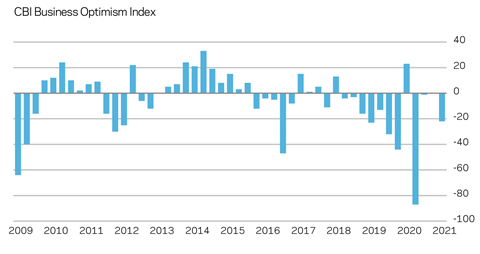

Business sentiment

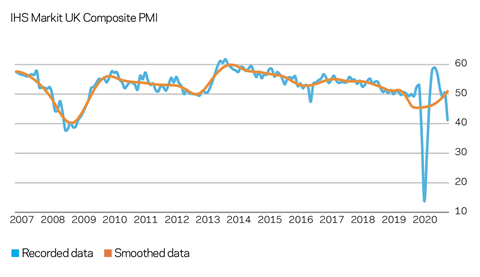

The UK’s GDP annual growth rate of -8.6% at Q3 2020 recovered from its largest ever fall, posted in the second quarter. The quarterly growth at Q3 posted its largest ever gain, at +16%. Context is important for this rebound, given the size of the decline in Q2 2020 and the impacts from the first lockdown. A double-dip recession looks highly likely as subsequent regional and national lockdowns further stifle economic activity. But the covid vaccination rollout will slowly provide some underlying economic stability, barring any impediments to the programme.

Negative risks to sentiment are provided by Brexit red tape and general uncertainty. There is much talk of an approaching inflection point, but the most recent lockdown and its unknown duration make economic recovery hard to predict. Brexit has introduced more complex trading conditions for almost all sectors, and amid the pressing concerns of carrying on day-to-day trading, the fundamental question for businesses is what this means for them in the medium term.

Business sentiment surveys are holding at or around long-run averages. However, confidence about the UK economy is something of a meringue: apparent firmness on the exterior but fragile beneath the surface. Brexit or covid alone would create an uphill struggle for the UK economy; together they steepen the incline. The construction sector is not immune, despite many sites remaining open through this latest national lockdown. Construction sector sentiment mirrored broader measures in posting historically significant falls, with sizeable rebounds following immediately afterwards. Projects paused as a result of the pandemic have started to filter back into the marketplace in the latter months of 2020, providing a fillip to activity.

Despite uncertainty elsewhere in the economy, reasonable levels of construction output are expected for 2021. Parts of the sector are insulated to some extent from immediate Brexit-related issues, but not those parts of project delivery that require imported materials and components. Sentiment will be inherently related to questions further out on the impacts of Brexit and how attractive the UK is to foreign direct investment or indeed domestic investment.

04 / Building costs

Inputs

Aecom’s composite index for building costs – comprised of materials and labour inputs – increased by 1.1% in the 12 months to Q4 2020, with almost all materials classifications in the index showing a rise. The cost index moved higher on the strength of quicker demand from catch-up activity, tight supply chain conditions in some parts, higher international logistics costs, and stockpiling for the then impending Brexit deadline. Consequently, the quarterly movement from Q3 to Q4 2020 saw a larger nominal increase at 1.9%. The largest increases were in timber products, particularly imported ones. Notable supply disruptions through 2021 are expected across many sectors, including construction, which will only add to the difficulties in procuring materials, goods and components. The CBI recently said around half of UK manufacturers are worried access to materials and components might limit their output over the next quarter – the highest level for this question in its survey since the 1970s. Delivery times have lengthened considerably too.

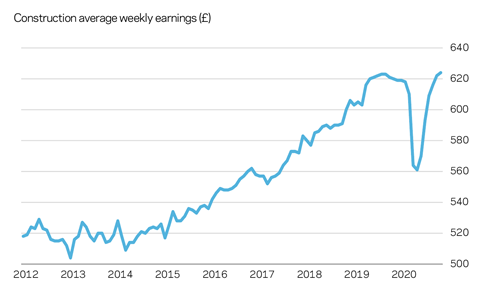

Aggregate wage levels continued to rise over Q4 2020 and into 2021, as renewed site activity increased workforce labour demand. However, wage inflation over the 12 months to Q4 2020 was flat to marginally negative. Migration trends out of the UK are further risks for the construction sector and its workforce.

Commodities prices also saw notable increases in the latter part of 2020. Various demand-side macroeconomic and industry-level factors are contributing to these recent commodities price increases. Nevertheless, a significant driver of the underlying trend in dollar-priced commodities is the weakening of the US dollar over the same period.

05 / Tender prices

Resources

An aggregate measure of tender prices decreased by just over 1% provisionally in the 12 months to Q4 2020. But assessing price trends over shorter timeframes, prices fell 1.6% between Q2 and Q3, and by approximately 0.6% between Q3 and Q4. Tender price inflation clearly slowed in 2020, with some trades offering much keener pricing. As with activity and sentiment measures, it was not a uniform picture though. Variance in pricing between tenderers has increased. This is an expected outcome in a market seeing higher levels of competition. Firms’ pricing responses depended on their commercial and financial position going into the coronavirus lockdowns and their levels of secured workload for 2021.

Risk mitigation through the first lockdown was notable. Commercial stability was achieved in quickly addressing risks as they arose, given the magnitude of the pandemic situation. Market dynamics through 2020 amplified the choices that supply chain firms needed to make in respect of input costs pressures and selling prices, though. Labour rates remain very responsive to monthly or quarterly changes in output, as do measures of industry capacity, which continue to indicate the structurally enduring problems of this issue. Even where demand has fallen away, inflationary pressures have not dissipated in the same proportion.

06 / Outlook

TPI forecast

Talk of so-called “new normals” last year and adjustments required because of the pandemic have morphed into questions about when normality will return. This is mostly on the back of the vaccine rollout. The second wave of the pandemic – with higher virulence now – introduces renewed risks for the construction sector, especially the longer that lockdowns continue. Social distancing restrictions on sites will continue to impact productivity, with output figures expected to eventually bear this out in published output data later in 2021.

For its voluminous page count, the Brexit Trade and Cooperation Agreement signed between the EU and UK at the end of 2020 is widely regarded as a thin or minimal trade agreement between the two parties, limited in its scope. Services, which are a substantial part of the UK economy, are largely excluded. For UK and EU companies – many of which provide materials, components and services for the UK construction sector – Brexit necessitates a recalibration of trade patterns and relationships and for businesses to navigate a profoundly different regulatory environment. Inevitably, this brings disruption – and unintended consequences.

That UK construction has a broadly domestic focus does offer some level of continuity. Nevertheless, visible implications from Brexit are likely for the sector soon. Using an operational example to illuminate the changed situation, construction plant and machinery with an EU link in its mechanical production and supply chain will see longer repair times and/or equipment downtime in the event of breakdown. Just-in-time or efficient transportation of equipment spare parts is much less certain now. Non-tariff barriers will introduce notably extended delivery times and additional costs. Knock-on effects are inevitable for construction programmes and completion dates as a result of longer repair durations, along with higher costs.

Larger businesses will be better able to absorb the substantial amounts of new and permanent red tape for importing and exporting. Some red tape is inevitable in trade, but more begins to act as sand in the engine of industry and commerce, impeding the efficiency of movement. Whether it affects a firm’s operations directly, or indirectly through the supply chain, will depend on the firm’s business model. SMEs will be disproportionally affected, with the red tape cost burden becoming a much larger percentage of their turnover and having a disproportionate effect on their cost base. Accompanying contractual risks for construction SMEs are also significant in the mechanical breakdown example. Nevertheless, the Brexit milieu is a deeply embedded inflationary component to costs and prices.

Aecom’s baseline outlook scenario sees an on-going slow economic recovery. There is little sign yet of government capital spending that directly benefits the construction sector. Public finances are in a very different position now. Nonetheless, the vaccine rollout programme provides a slow underpinning of the economy to some extent. Competing inflationary and deflationary pressures are clear. Commercial pressures are expected from renewed input cost inflation – both materials and labour costs. Non-tariff barriers introduced by Brexit will now add additional costs into the supply chain. Irrespective of whether these are inflationary cost pressures directly for supply chain firms, or indirectly from their suppliers, they are further commercial strains when the market is already more competitive. Deflationary pressures come from a likely double-dip recession and economic sluggishness. This influences the level of overall construction demand, especially in non-housing construction subsectors. But it is notable that for the substantial falls in output last year, tender prices have not fallen by any proportional amount. This is reflective of the capacity constraints that afflict the construction sector. What were cyclical issues historically are now clear structural problems for the industry.

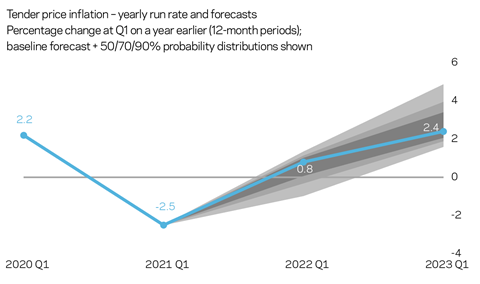

Any increases in new orders and output will feed into tender pricing movements quite quickly. For now, tender prices are forecast to increase by 0.8% from Q1 2021 to Q1 2022, and 2.4% from Q1 2022 to Q1 2023. Notable downside risks apply to the first 12-month period, which the confidence intervals reflect. The second 12-month forecast period sees higher optimism, introducing greater upside risks over that period.

No comments yet