A month on from the Budget, the construction sector remains in reasonable health despite monthy fluctuations. Michael Dall discusses the highlights of Barbour ABI’s monthly Economic & Construction Market Review

Economic context

Last month saw the first sole Conservative Budget since 1997 announced.

It set the course of further austerity over the course of this parliament, with the projection that the UK deficit will be eradicated by 2018/19. The majority of headline measures focused on income tax threshold changes and a new proposed “sugar tax” on confectionery and fizzy drinks.

The Office for Budget Responsibility (OBR) updated its economic forecasts for the UK in the upcoming years with its estimate for growth this year now 2.0%, down from the 2.4% forecast in the Autumn Statement. The forecast for 2017 was also revised downwards with an estimate of 2.2% growth, a decrease from the 2.5% figure predicted in December. The OBR now thinks that growth will continue at 2.1% from 2018 until 2020.

Inflation forecasts were also reduced for 2016 from 1.0% to 0.7%, which is significantly below the target of 2.0%. The OBR’s inflation target of 2.0% is predicted to be met in 2018, a year earlier than the Autumn Statement predicted.

It is clear that the main reason for the fall this month was the reduction in industrial activity, which declined by 9.7% compared to Feb 2015

Average earnings growth forecasts were revised downwards, with the OBR revising its forecasts to 2.6% wage growth this year, when it expected the figure to be 3.4% when the Autumn Statement was announced. Wages are therefore forecast to rise above the level of inflation this year and this is forecast to continue for the rest of period, with average earnings growth of 3.6% estimated in 2020.

Unemployment forecasts remained positive in the Budget, with downward revisions since the Autumn Statement. Unemployment in 2016 is estimated to be 5.0% this year, remaining at that level in 2017. It is then set to rise to 5.3% in 2019 and stay at that level in 2020.

The many policy measures announced in the statement included:

- Extra £700m announced for flood defences

- £300m for transport projects

- More than £230m earmarked for road improvements in the north of England

- The delivery of 13,000 affordable homes two years early by bringing forward £250m of capital spending to 2017-18 and 2018-19

- Starter Homes Land Fund prospectus inviting local authorities to access £1.2bn of funding to remediate brownfield land for housing

- Consultation on increasing transparency in the property market

- HCA working with Network Rail on releasing land for housing and commercial schemes

- Legislation to make it easier for local authorities to work together to create garden towns

- East Anglia and the west of England (Bristol and Bath) to get combined authorities

- Osborne has opened negotiations with Edinburgh and Swansea over new City Deals

- The carbon reduction commitment – a mandatory emissions reduction scheme for large organisations – has been scrapped

- Stamp duty reform for commercial properties

- Small businesses will be exempt from business rates up to £15,000 in revenue, and 600,000 small businesses will pay no rates at all

- Corporation tax to be cut to 17% by 2020

The construction sector

The construction sector remains in fairly rude health despite monthly fluctuations.

The Construction Products Association recently updated its forecasts for 2016 and beyond and the industry is now predicted to grow by 3.6% this year and 4.1% next year on the back of continuing strength in the new build residential sector and increasing activity in the commercial and infrastructure sectors.

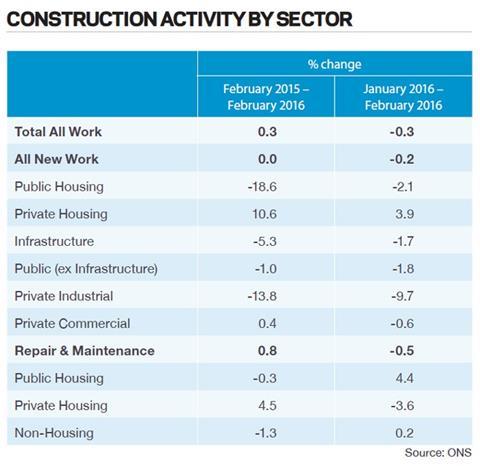

The latest figures from the ONS show that the construction sector in the UK declined by 0.3% between January and February 2016. Comparing February output levels with the same month in 2015 showed an increase of 0.3% (see Construction Activity By Sector). This fall was unexpected but it should be noted that the monthly figures for construction output are often volatile and the previous three months’ data had been significantly revised upwards.

It is clear that the main reason for the fall this month was the reduction in industrial activity, which declined by 9.7% compared to February 2015 and 13.8% compared to January 2016. New private housing increased by 10.6% from February 2015 and was up by 3.9% compared to January 2016. Public housing output declined by 18.6% compared to February 2015 and 2.1% compared to January 2016, though this is a significantly smaller sector than private housing. This highlights that the growth patterns within the industry are still reliant on private housing.

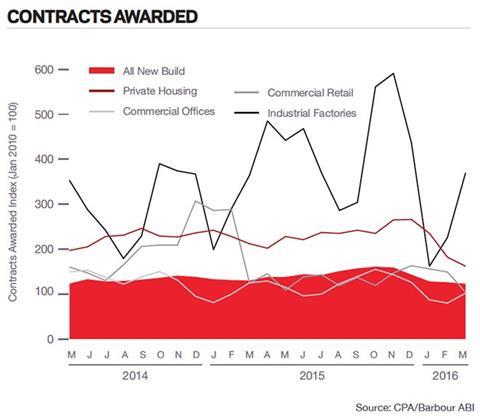

The CPA/Barbour ABI Index, which measures the level of contracts awarded using January 2010 as its base month, recorded a reading of 123 for March (see Contracts Awarded). This is slightly down on last month but supports the view that overall activity in the industry remains strong.

According to Barbour ABI data on all contract activity, March witnessed an increase in construction levels, with the value of new contracts awarded at £6.1bn, based on a three-month rolling average. This is a 9% increase from February and a 1.7% decrease on the value recorded in March 2015. The number of construction projects within the UK in March decreased by 4.7% on February, and were 1.2% lower than March 2015.

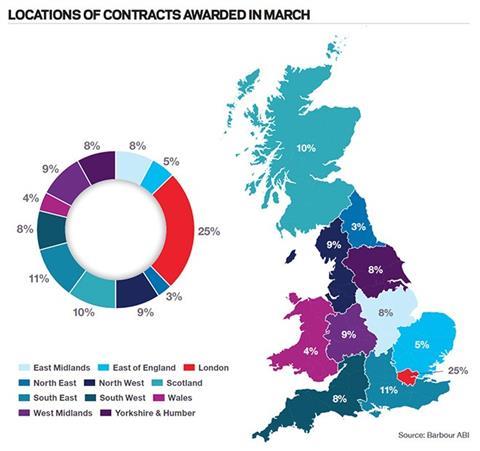

Projects by region

The majority of the contracts awarded in March by value were in London, accounting for 25% of the UK total. This is followed by the South-east with 11%. The main reason for London’s figures this month was the award of the engineering partner for the HS2 scheme, valued at £350m.

Types of project

Residential had the highest proportion of contracts awarded by value in March with 31% of the total. The infrastructure sector accounted for 24%.

This is an indication of the continuing strength of the residential sector within construction, showing that while the top end of the residential market appears to be cooling, activity in the new build market remains strong.

Construction performance by sector

Spotlight on residential

Activity in the residential sector increased in March with the total value of projects valued at £1.9bn based on a three-month rolling average. This is a 6.4% increase compared to February and is 0.8% higher than March 2015. The number of units associated with residential contracts awarded decreased 3.5% between February and March based on a three-month rolling average, and is 32.3% lower than March 2015.

Sector performance

The latest house price indices for March from Nationwide showed that average house prices are rising at 5.7% annually, an increase from 4.8% in February. The Halifax reported annual house price rises at 10.1% in March, up from 9.7% in February.

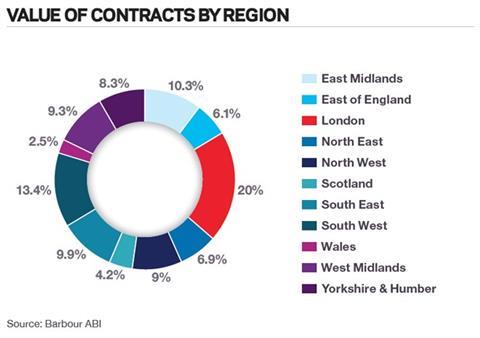

Projects by region

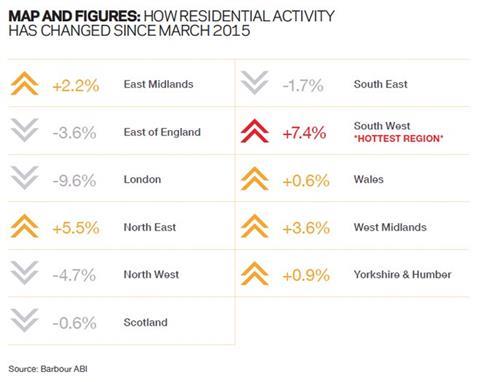

London is the main location of activity in the residential sector this month, accounting for 20% of the value of contracts awarded, a decrease of 9.6% from the same month last year. The South-west had the next highest proportion of contract award value in March with 13.4% of total value awarded, an increase of 7.4% from March 2015.

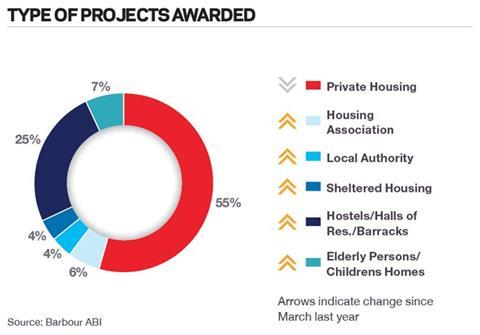

Type of projects

The type of projects awarded in the residential sector was dominated by private housing this month. Private housing accounted for 55% of the value of contracts awarded this month, a decrease of 25% from March last year. After private housing, the next largest project type were hostels, which accounted for 25% of the value awarded, an increase of 6% from this time last year.

No comments yet