July saw construction activity levels pick up, in a reflection of the wider economy during the spring months. Michael Dall discusses the highlights of Barbour ABI’s monthly Economics & Construction Market Review

Economic context

The latest GDP figures for the UK economy were released in the last month and they showed that the UK economy had grown by 0.7% in the second quarter of 2015.

This was above the 0.4% rate of growth experienced in the first quarter of 2015 and is an indication that the economy regained its momentum over the spring months.

While the total level of output is now comfortably above its pre-recession peak, the pattern of growth within the economy is still very much focused towards the dominant service sector. The latest figures show that the service sector is now 9.2% higher than its pre-recession peak and construction is currently 3.2% below its pre-recession peak, while manufacturing is 4.9% below. This indicates the scale of the challenge of rebalancing the economy towards manufacturing and construction given the prominence of the service sector.

The labour market continues to perform particularly strongly in the UK. However, it is notable that there has been a slight increase in the levels of unemployment over the past two months. The rate of unemployment is currently 5.6% for those aged 16 and over, up from 5.5% in March 2015.

The main reason for the quarterly increase in output is increases in new private housing and new infrastructure

The rate of inflation was 0.1% in July with the continued decline in oil, clothing and food prices the main reasons for this. Most commentators expect inflation to start growing towards the end of the year as these falls will be factored into the yearly change figures.

Other news this month on the UK economy includes:

- A survey by the CIPD showed that one-third of the 900 companies asked planned to recruit apprentices, up from 22% last year

- The latest Inflation Report from the Bank of England concluded that the outlook for growth in the UK was strong, and upgraded its growth forecast to 2.8% for 2015

- A survey by Nielsen showed that UK consumer confidence was above the global average for the first time since 2006

The latest figures from the ONS indicate the construction sector in the UK grew by 0.2% between Q2 2015 and Q1 2015.

Comparing Q2 output levels with the same period in 2014 showed an increase of 2.4%. The decline consisted of a flat April, decline in May, but growth in June.

The main reason for the quarterly increase in output is increases in new private housing and new infrastructure. New private housing increased by 11.6% compared with Q2 2015 and infrastructure increased by 16.7% over the same period. However, the commercial sector declined by 0.3% over the quarter and by 1.2% compared with the second quarter of 2014, which has proved a drag on overall growth (see Construction activity by sector, right).

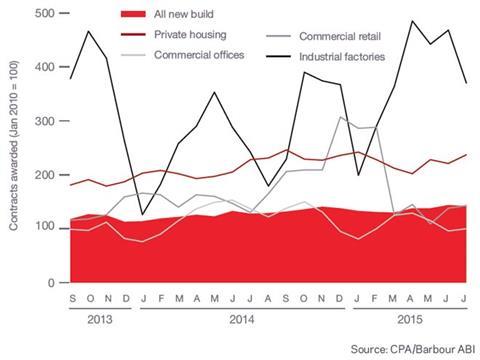

The CPA/Barbour ABI Index, which measures the level of contracts awarded using January 2010 as its base month, recorded a reading of 142 for July. This is an increase from the previous month and continues to support the view that overall activity in the industry remains strong. The readings for private housing increased in the month after a slight decrease in June. Commercial offices increased with a reading of 100 compared to 96 last month. However, commercial retail increased in July with a reading of 143 although industrial factories recorded a reading of 370, down from 468 in June (see Contracts awarded, right).

The construction sector

According to Barbour ABI data on all contract activity, July witnessed an increase in construction activity levels with the value of new contracts awarded £6.5bn, based on a three-month rolling average.

This is a 5% increase from June and a 28.7% increase on the value recorded in July 2014. The number of construction projects within the UK in July increased by 8.1% on June, but were 11.7% lower than July 2014.

Projects by region

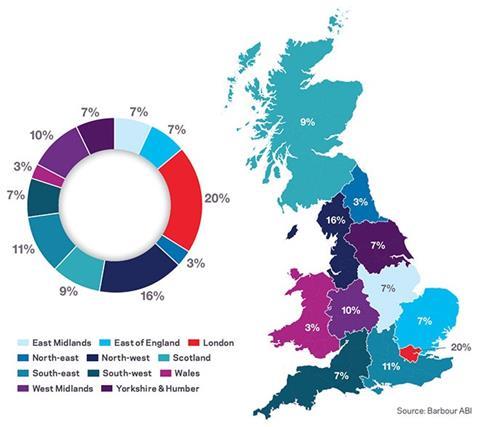

The highest proportion of the contracts awarded in July by value were in London, accounting 20% of the UK total. This is followed by the North-west with 16% of contract value awarded and the South-east with 11% of value (see Locations of contracts awarded, right). The strong performance of London is primarily due to the award of the £300m contract at 22-24 Bishopsgate. This major commercially led project will also provide retail and leisure uses and is the second major contract of its type awarded this summer after Wood Wharf in June. In the North-west a major renewable energy project, the Burbo Bank offshore wind farm extension, was the highest value contract awarded in July. This contract has an estimated value of £250m and is due to be completed over two years.

Type of projects

Infrastructure had the highest proportion of contracts awarded by value in July with 27% of the total value of projects awarded, keeping it in line with its strong performance in recent months. Renewable energy projects were the main factor in its strong performance with the Burbo Bank offshore wind farm and energy-from-waste facility in Beddington worth £200m both awarded in July. The residential sector also had a strong month in July, accounting for 26% of the value awarded.

Locations of contracts awarded in July

Contracts awarded

Construction activity by sector

| % change | ||

|---|---|---|

| Q2 2014 – Q2 2015 | Q1 2015 – Q2 2015 | |

| Total all work | 2.4 | 0.2 |

| All new work | 5.2 | 1 |

| Public housing | -7 | -2.5 |

| Private housing | 11.6 | 3.9 |

| Infrastructure | 16.7 | 0.5 |

| Public (ex infrastructure) | -0.5 | 1.2 |

| Private industrial | 0.7 | -1.5 |

| Private commercial | -1.2 | -0.3 |

| Repair & maintenance | -2.2 | -1.2 |

| Public housing | -1 | -0.4 |

| Private housing | 2.2 | 2.4 |

| Non-housing | -5.4 | -3.9 |

Construction performance by sector

Spotlight on infrastructure

Renewable energy and road projects awarded in the month saw the value of infrastructure contracts increase and values significantly higher than this time in 2014.

The value of contracts awarded increased in July with a total value of £2bn based on a three-month rolling average. This is a 17.6% increase from the previous month and is 88.5% higher than July 2014. In the three months to July the total value of contracts awarded was £5.6bn based on a three-month rolling average. This is 34% higher than the previous three months and 67% higher than the same period in 2014. This indicates a significant improvement on last year and is potentially a boost to overall growth in the construction industry should it continue.

Projects by region

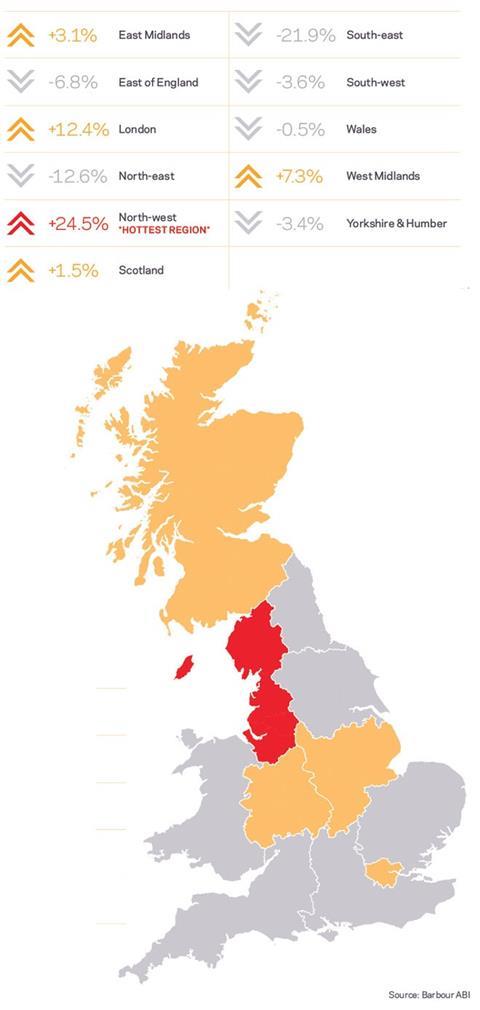

The North-west dominated infrastructure contracts in July, accounting for 32.4% of the value awarded, a 24.5% increase on July 2014. London was the second most prominent location in July with 16% of contract value, a 12.4% increase from June 2014.

Type of projects

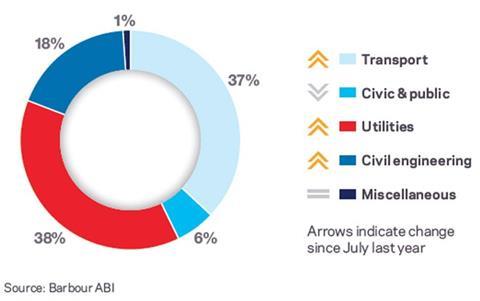

The offshore wind farm contract at Burbo Bank, alongside other renewable energy contracts, means that utilities is the sub-sector with the highest share of contracts awarded. Utilities accounted for 38% of the value of contracts awarded in July, an increase of 1% from July last year. Continued spending on roads means that transport received 37% of the share of contracts awarded in July, an increase of 9% from 2014.

Maps and figures: How infrastructure activity has changed since July 2014

Type of projects awarded

Value of contracts by region

Top 10 key clients: Aug 2014–Jul 2015

| Company name | Awards | Value (£m) | |

|---|---|---|---|

| 1 | Highways England | 74 | 1,581 |

| 2 | Transport Scotland | 9 | 1,164 |

| 3 | Aberdeen City council | 7 | 1,087 |

| 4 | Welsh Assembly Government | 4 | 820 |

| 5 | Battersea Power Station Development Company | 1 | 600 |

| 6 | Scottish Government | 1 | 530 |

| 7 | Network Rail Infrastructure | 74 | 342 |

| 8 | Environment Agency | 19 | 233 |

| 9 | Viridor Waste Management | 1 | 200 |

| 10 | TFGM | 2 | 172 |

Top 10 key contractors: Aug 2014–Jul 2015

| Company name | Awards | Value (£m) | |

|---|---|---|---|

| 1 | Aberdeen Roads | 5 | 1,060 |

| 2 | Vinci Construction UK | 17 | 884 |

| 3 | Costain/Skanska JV | 2 | 600 |

| 4 | Ferrovial Agroman Laing O’Rourke JV | 1 | 600 |

| 5 | Balfour Beatty Group | 42 | 557 |

| 6 | VolkerWessels UK | 25 | 254 |

| 7 | Lagan Construction Group | 1 | 200 |

| 8 | Costain and Carillion JV | 1 | 162 |

| 9 | Carillion | 9 | 144 |

| 10 | Amey Group | 6 | 131 |

Downloads

ECMR August 2015

PDF, Size 0 kb

No comments yet